English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  French (Canada)

French (Canada)

bfinance insight from:

Martha Brindle

Director, Equity

Sarita Gosrani

Director, ESG

With the investment industry expecting significant outcomes from COP26 in November, climate risk management and portfolio carbon exposures have never been higher on investors’ agendas. Here, we examine today’s rapidly changing menu of climate-aware equity strategies, which revolve around two (potentially conflicting!) themes: reducing carbon emissions and supporting the transition to a low-carbon economy.

This article is the first instalment in a three-part series. Part 3—Feeling the Heat? Taking the Temperature of Equity Portfolios—can be viewed here.

This year has brought a surge in collaborative action intended to tackle climate change, including Net Zero commitments and announcements from across the institutional investment industry. September brought the launch of the Net Zero Investment Consultants Initiative, in which thirteen founding firms with an AuA of more than US$10 trillion—including bfinance—set out clear commitments in this space. Meanwhile, more than 40 asset owners have now committed to Net Zero through the UN-convened Asset Owners Alliance, and the Net Zero Asset Managers Initiative has garnered over 100 signatories with more than USD40 trillion in AuM.

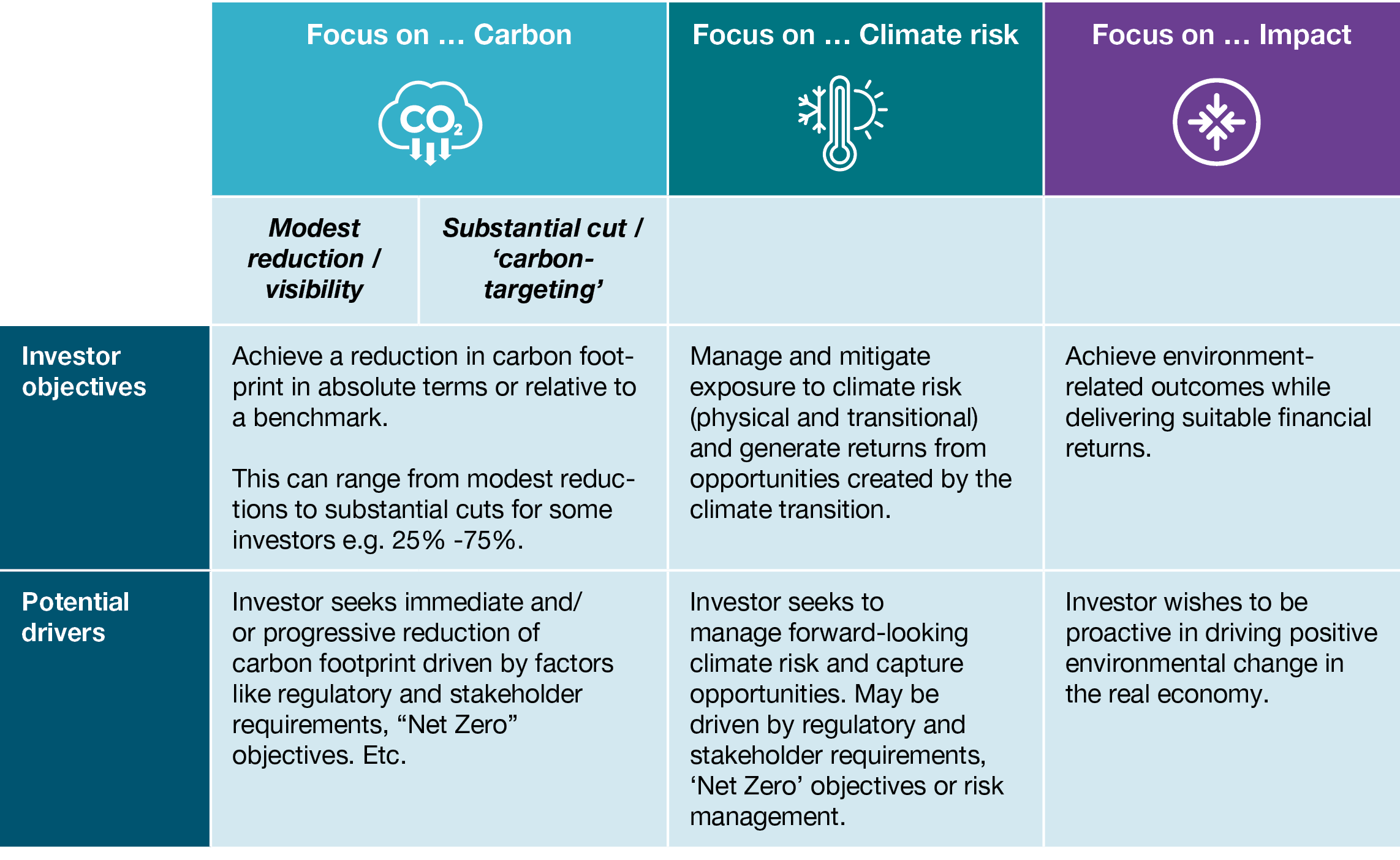

Investors are increasingly seeking to understand the impact of climate risk within portfolios and take action. Motivations may be both intrinsic and extrinsic: regulatory pressure, data accessibility, stakeholder interest and investment product availability all play a role, alongside the now-widely-accepted premise that climate risk is systemic and financially material for long-term investors. At bfinance, we now see clients targeting a wide variety of objectives in this space, as illustrated in Figure 1. Today, the focus appears to be shifting from measuring and reducing carbon emissions towards gaining a better understanding of forward-looking climate risk.

FIGURE 1: INVESTOR OBJECTIVES AND POTENTIAL DRIVERS

Equities in focus

In this article, we look at the current range of strategies available in listed equities—a product universe which has changed considerably in recent years—and address key issues such as data shortcomings, style/sector exposures and manager selection challenges. Equity portfolios sat on the front line for the early waves of ESG activity in the investment industry; today, thanks to data availability, this asset class is typically the first to receive attention when investors turn towards the subject of carbon emissions – as illustrated in a recent series of interviews with Nordic and Dutch investors.

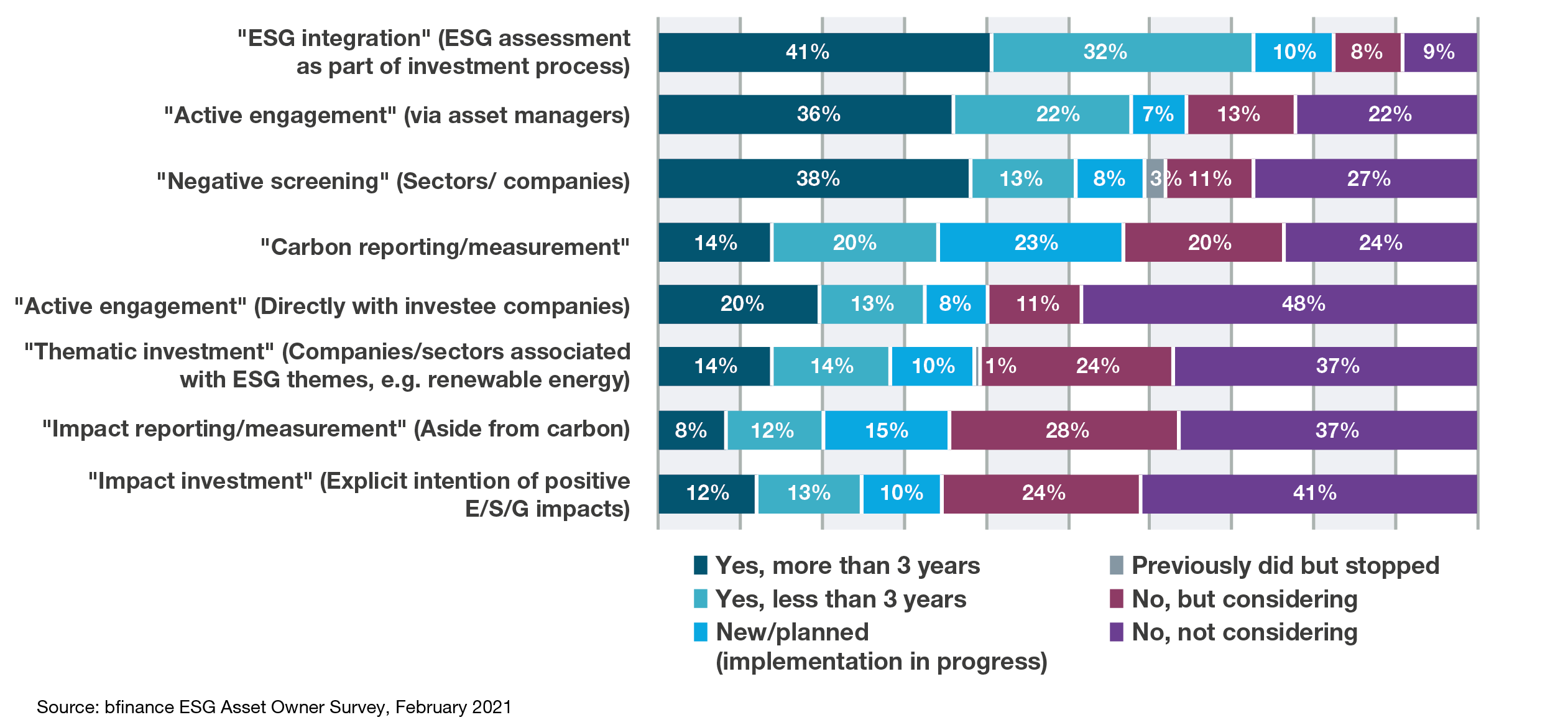

A quarter of new equity manager searches in the last year have targeted a reduction in the portfolio’s carbon intensity.

FIGURE 2: WHICH OF THE FOLLOWING ESG APPROACHES DO YOU USE IN EQUITIES?

While the vast majority of bfinance clients now apply ESG criteria when appointing new equity managers, climate change considerations are moving up the agenda: approximately a quarter of new equity manager searches in the last year have targeted a reduction in the portfolio’s carbon intensity and nearly one in six have explicitly considered Net Zero alignment.

Climate-aware equity strategies: an overview

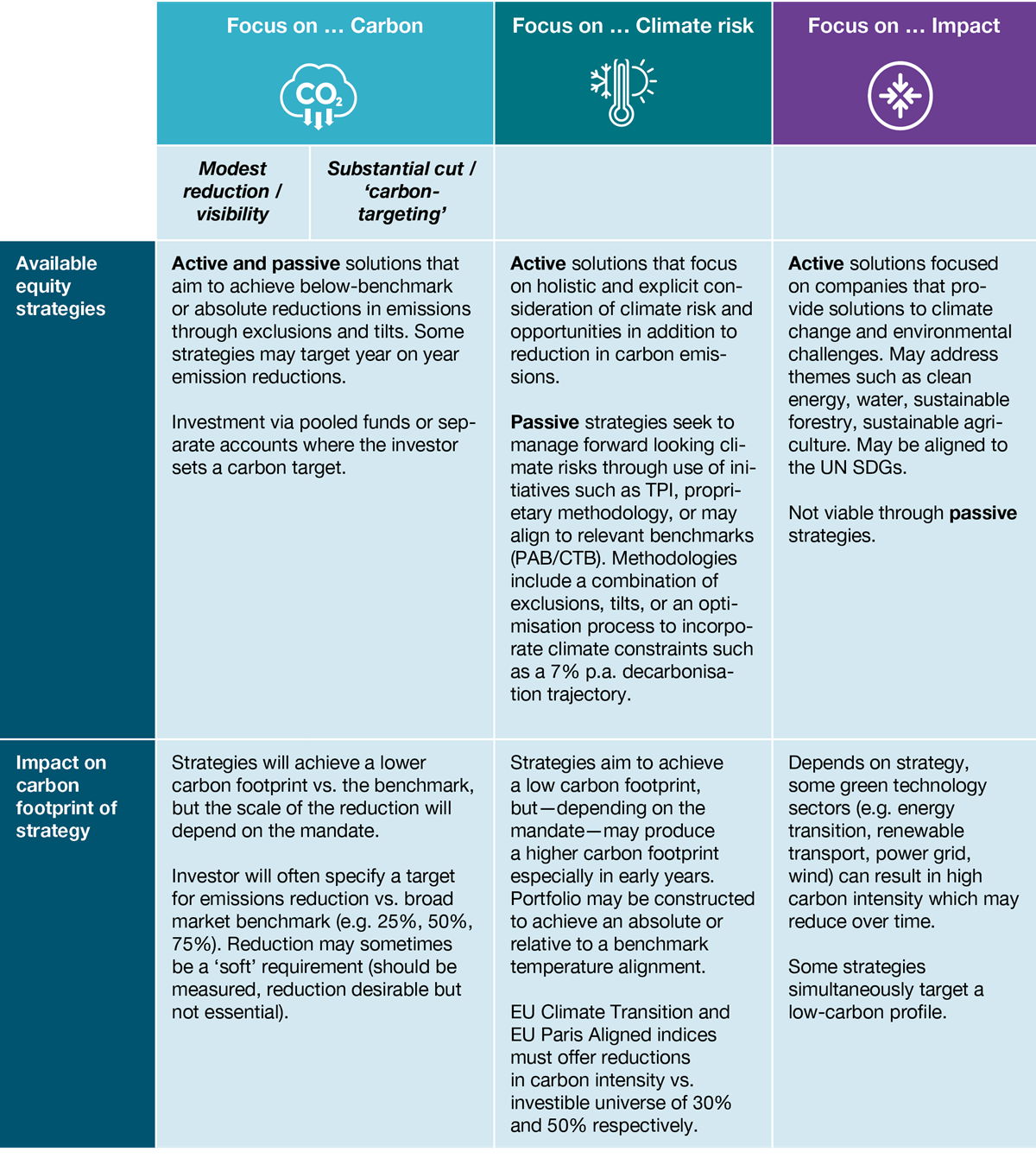

Our recent research highlights well over 60 active listed equity strategies available to institutional investors that are explicitly focused on carbon or climate change considerations (readers should note that this figure does not include passive or semi-passive strategies). This is a growing segment, but still relatively new: funds typically have relatively short track records. In addition, many more equity managers are able to provide reductions in carbon intensity as an overlay to their conventional strategies via separate accounts—this latter requirement can usually be easily implemented by investors without significantly reducing the number of strategies that would otherwise be available. Figure 3 provides some details on the relevant strategies, matching them to the investor objectives described in Figure 2.

FIGURE 3: AVAILABLE EQUITY STRATEGIES AND IMPLICATIONS FOR CARBON EMISSIONS

Each of these approaches brings their own advantages, disadvantages and investment implications. In the discussion below, we consider a few of the key issues.

Category 1: ‘Focus on carbon’ — strategies explicitly designed to reduce emissions

These strategies—active or passive—represent an effective way to materially reduce portfolio carbon footprints and mitigate exposure to high emitters, predominantly focusing on carbon emissions and fossil fuel reserves. Strategies in this category typically provide impact on portfolio carbon intensity from day one and may be followed by a progressive decrease over time.

An important consideration for these strategies is how the carbon objective may influence overall portfolio exposures (e.g. sector and style). Active strategies may be underweight energy and overweight sectors such as technology, software and healthcare. Portfolios may also be relatively concentrated, depending on the extent of reduction required and the investment approach. There are different methodologies for achieving a carbon reduction target, with different effects on portfolio composition.

Carbon data challenges remain

Carbon data is readily available from a variety of sources, thanks to regulatory pressure, investor demands and initiatives such as CPD and TCFD. Yet there are still several areas of difficulty:

> Coverage: Scope 1 and 2 emissions are widely available; Scope 3 emissions (which can account for more than ¾ of a firm’s emissions) are often omitted or unavailable but can significantly change the picture. Emerging markets coverage is low.

> Verifiability: Data is not easily verifiable due to the lack of standardisation and can be problematic for firms with complex structures. There are global initiatives targeting this issue (e.g. IFRS).

> Consistency: There remains a disparity between methodologies used to calculate carbon metrics. This issue is exacerbated by disparities between data providers.

> Timeliness: Data is lagged and backward-looking; does not address forward-looking climate risk.

> Usage: While the quality of data is an important subject, it is often more important to understand how the available data is being used in the management of assets.

Investors in this space should remember that carbon emissions data on its own does not indicate a company’s future path or wider commitment to addressing climate change; the data used is inherently backward-looking and static. This type of strategy may also limit the investor’s influence over companies that will be more relevant to the transition, and (therefore) their potential to generate impact.

Category 2: ‘Focus on climate’ — strategies that manage and mitigate exposure to climate risk

There is now a rapidly growing universe of active and passive products that consider climate risk: recent product launches have chiefly sat in this part of the spectrum, rather than looking solely at carbon reduction. These climate strategies espouse a holistic approach, incorporating both emissions data and analysis of a company’s trajectory into decision-making. This is intended to enable investors to capture opportunities created by climate change while also incentivising companies to put transition strategies in place. It is, one could argue, an approach which is more intellectually aligned with the TCFD philosophy. Strong active stewardship programmes are often crucial to these strategies, driving the introduction of climate-related targets among investee companies alongside the overall transition of their operations towards alignment with a low-carbon economy.

It is important to note that these climate strategies may result in higher carbon footprints than the strategies in the prior group—especially in earlier years—since they can hold companies that may be high emitters but demonstrate a commitment to transitioning to a low carbon economy. Some of these strategies do simultaneously target below-benchmark carbon emissions, but this is not the case for all.

The challenges associated with carbon data are illustrated above. The datasets for forward looking climate metrics are even more nascent. Even well-respected metrics such as those from the Science Based Targets Initiative (SBTi) were still developing through 2020, while TruCost announced its Paris Aligned data set less than a year ago, in December 2020. Temperature alignment metrics and risk measurement tools such as scenario analysis are also evolving. Investors should expect significant refinement in methodologies as well as improving coverage. In the interim, however, it is important to understand the approaches being used by external asset managers. Active managers in this group often seek to avoid relying solely on external datasets without additional in-house assessment.

Other notable challenges when investing in this space include short track records and an evolving regulatory and fund taxonomy that can make it difficult for investors to compare strategies. Hurdles notwithstanding, we do now view this group as offering a highly credible opportunity for investors seeking to capture climate risks and support the energy transition.

Category 3: ‘Focus on impact’ — strategies with the intention of delivering environmental benefit alongside financial returns

Strategies that focus on impact are designed to generate financial returns while capturing opportunities created by climate change and the transitioning economy in a more concentrated and explicit way than we have seen in the prior group. Both, however, could be described as impact strategies in that they share the aim of reducing emissions in the real economy.

Here we see a more concentrated focus on companies that can provide solutions to the existing environmental challenges thereby focusing on themes such as the clean energy transition, water, biodiversity, sustainable forestry, sustainable agriculture and so forth. While sector skews may be evident in the previous group, here they are expected. From a portfolio style perspective, these strategies are likely to have a strong tilt towards growth, with companies bringing out innovative (or even disruptive) products and technologies to solve environmental challenges.

Investors in these strategies generally seek tangible outcomes that can be quantified and communicated to stakeholders. Managers must engage with companies on their impact progress and provide appropriate reporting. Although measurement is not straightforward, the methodology and metrics surrounding impact are evolving rapidly.

Conclusion: a careful approach towards managing climate risk

We view investors’ growing focus on climate risk as an extremely positive shift—for risk management, for investment opportunity, and for the planet at large. Investment strategies are proliferating. Data and metrics are improving. And, notwithstanding the heightened incentives for ‘greenwashing’, asset managers’ products, methodologies, stewardship programmes are evolving in some innovative and interesting ways. These developments are also immensely helpful in supporting us, as advisors, in helping investors to take a robust approach to climate risk—whether pursuing an explicit Net Zero ambition or simply exercising good risk management. Yet investors must also be cautious and select objectives, strategies and managers with care. Carbon or climate-related objectives can have crucial consequences for portfolio exposures as well as environment-related ambitions.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.