English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  French (Canada)

French (Canada)

bfinance insight from:

Toby Goodworth

Managing Director & Head of Liquid Markets

‘Divergent’ or ‘convex’ hedge fund strategy indices posted average returns of nearly 10% through the first three quarters of 2022. Even small allocations to these strategies have provided investors with material improvements to their overall risk-adjusted returns and drawdown profiles – plus capital that can be re-deployed into traditional markets at attractive entry points. Is it time for investors to re-evaluate their hedge fund portfolios, or indeed make the move to create one?

As we take the time to reflect on the downturn of 2022, during which both core portfolio building blocks—equities and fixed income—delivered materially negative returns, ‘diversifiers’ are under scrutiny. Just as the Global Financial Crisis of 2008 informed a decade of portfolio design philosophy, the 2022 downturn will doubtless influence long-term strategic decisions in the decade to come. Private markets strategies have provided resilience so far, but a substantial proportion of that protection derives from delayed (and non-market-based) valuations: investors are still awaiting the full picture. As such, diversifying strategies in ‘liquid’ markets—such as hedge funds, Alternative Risk Premia and commodities—are receiving close attention.

How will hedge funds hold up under that microscope? A casual onlooker might assume that this sector has delivered somewhat unimpressive performance through recent market turmoil. According to the HFRI indices—the widely recognised industry benchmarks developed by the Hedge Fund Review—the average hedge fund has delivered moderate losses for the year to date. Overall asset-weighted performance was -6% for the first three quarters (-4.8% at the time of writing). The figure can hardly be considered successful for an investment style that, on the face of it, targets absolute returns. A closer look the data, however, reveals a different picture.

THREE HEDGE FUND TYPES

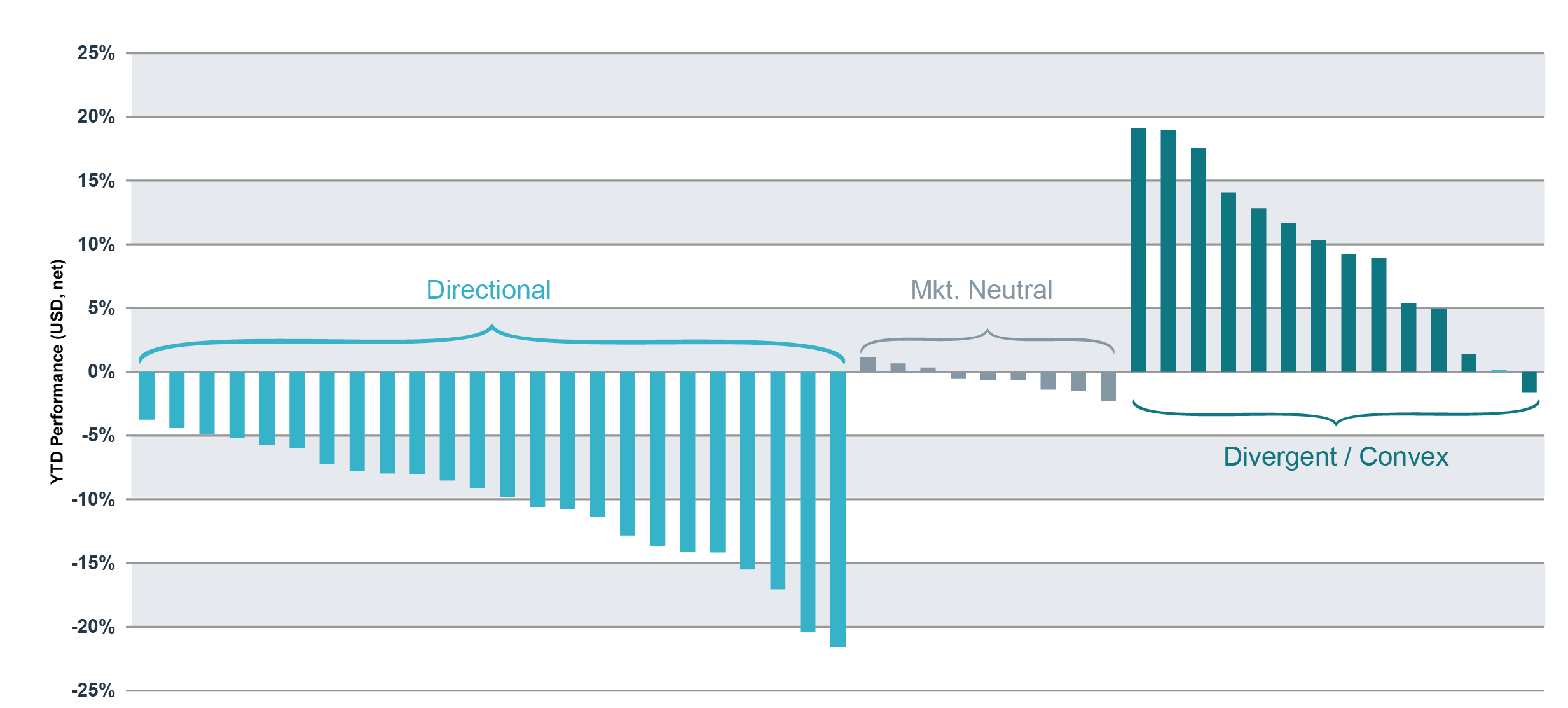

Three consecutive negative quarters for traditional risk assets have now provided a clear stratification of three hedge fund types: ‘Directional’, ‘Market Neutral’ and ‘Divergent/Convex’ – as shown in the chart below.

Figure 1: Performance of HFRI indices Jan-Sept 2022, categorised by type (net of fees)

Source: bfinance, HFRI. Each column represents the performance of one HFRI strategy index from January 1 2022 to September 30 2022. Indices are assigned to one of three categories by bfinance (listed in Appendix below).

For much of the post-GFC decade, on-paper performance did not showcase the very real distinctions between these groups (discussed here): a broadly benign macroeconomic and market environment meant that more conservative directional strategies seemed to overlap with their market-independent peers, while returns for macro and CTA strategies were muted.

In the recent period, which has brought some of the most extreme conditions witnessed since 2008, we can now clearly see these differences coming into focus (notwithstanding the essential caveats: short-term performance is not representative of longer-term results, and indices mask plenty of manager-specific performance dispersion). The ‘directional’ strategies have slumped, with average returns of -10.4% net of fees, although the losses are materially less severe than those of long-only equities or bonds. ‘Market independent’ strategies have lived up to the name, with (on average) broadly flat performance. Meanwhile, the ‘convex/divergent’ strategy indices have all delivered materially positive returns, with an average figure of 9.5% net of fees, thanks to explicit or implicit long-volatility positions (implicit in the case of managed futures). Trend-following strategies are having a particularly outstanding year—their best since 2008 in fact—off the back of a solid 2021.

These hedge fund groupings were set out in a mid-2021 white paper, How to Build a Hedge Fund Allocation, which encouraged the use of such categorisation when building or evaluating portfolios. Directional, market-independent and convex or divergent strategies all play different roles. ‘Market independence’, for example, may entail long-term diversification, but it should not be confused or conflated with ‘convexity’ – the specific ability to deliver good results when traditional risk assets are struggling. Portfolio construction should reflect those distinctions, with most institutional investors’ objectives making various types of diversification (not pro-cyclical alpha generation) the priority. Among bfinance’s client base, it’s worth noting that hedge fund manager search activity throughout the past two years has been heavily concentrated on either market-independent or divergent strategies, or (more recently) market-independent strategies with convex components.

Investors may now consider: do we have—or do we want—long-term exposure to strategies that are convex/divergent or market-independent or both? If so, how should portfolios be constructed with an appropriate balance of exposures to these types? Data from our recently published Global Asset Owner Survey suggests that a fresh look may be warranted. Some 69% of asset owners with hedge fund investments were ‘very’ (18%) or ‘quite’ (51%) satisfied with the performance delivered by their hedge funds in 2022 year-to-date — solid figures, but considerably lower than the 90%-plus of investors that expressed satisfaction with their private market investments.

For many investors, ‘hedge funds’ or ‘liquid alternatives’ or ‘diversifying strategies’ form a slice within a high-level strategic asset allocation and the allocation is typically assigned some sort of absolute or real return target. Yet it is critically important to ensure that the underlying mix is suitable for the investors’ true objectives for this allocation. Diversifiers and pro-cyclical alpha generators may both seek positive absolute returns, but they are extremely different in practice.

Constructing a liquid alternatives portfolio need not be daunting. With clear goals, it is not necessary to take something from every shelf in the alternative investment supermarket. Investors can, instead, target the correct tools for the job.

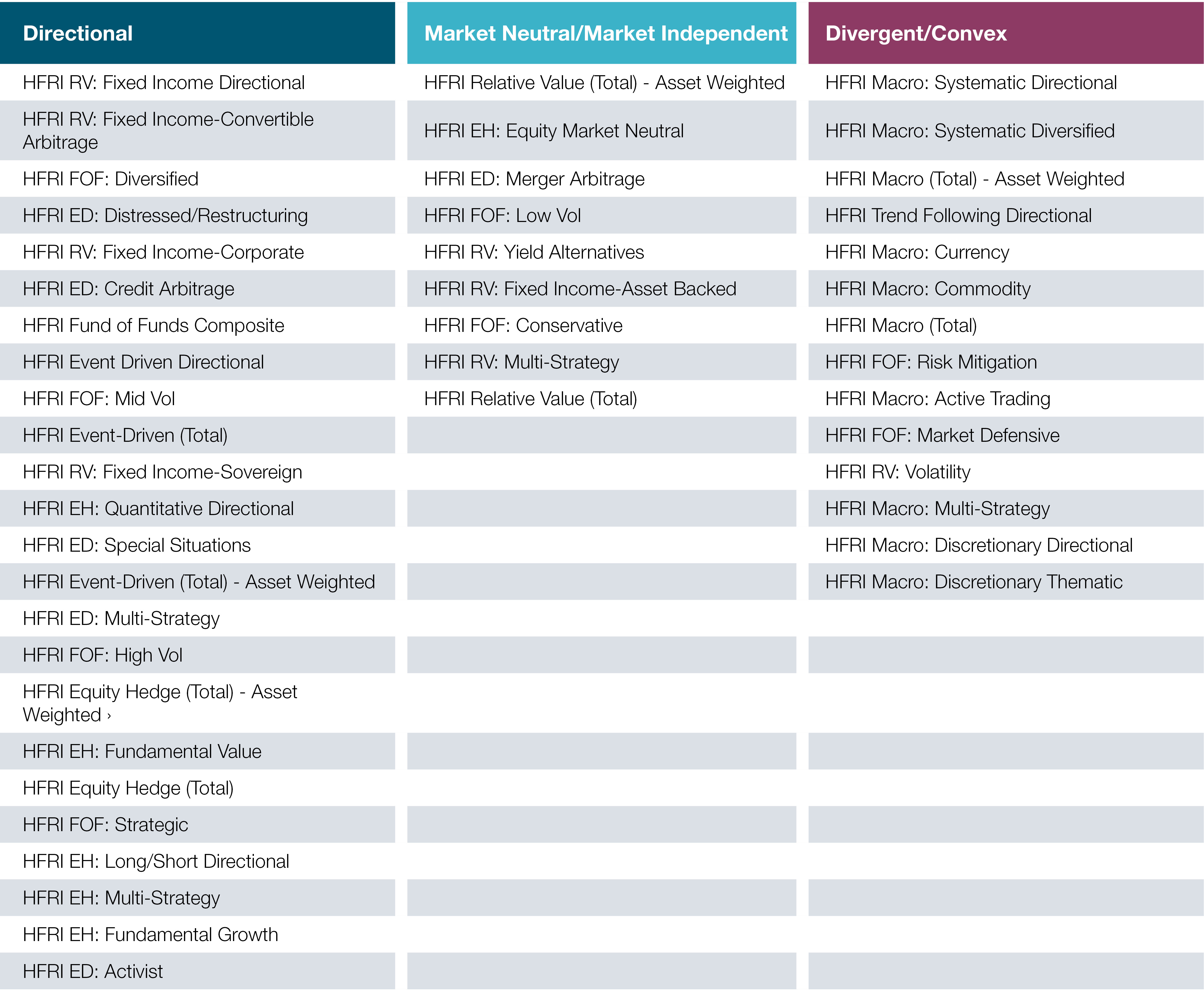

Appendix: bfinance classification of HFRI indices used in Figure 1

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.