English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  French (Canada)

French (Canada)

bfinance insight from:

Gerald Wu

Associate, Private Markets

Anish Butani

Senior Director, Private Markets

With diversity becoming an increasingly visible priority for investors, how do asset managers measure up? In this article we take a closer look at infrastructure managers, where recent searches highlight key diversity indicators and important nuances to watch out for.

Asset managers in both private and public markets are increasingly integrating a range of ESG factors within investment strategies. Yet diversity, whether that be the manager’s own diversity or how the subject is handled within the investment process, is still often treated as an afterthought in the broader ESG picture, buried within the “G” or “S” criteria.

This subject does, however, appear to be rising in prominence as a distinct theme in its own right across the international investor community. Asset owners in Africa, Australia, North America and Europe are actively considering diversity as part of their manager selection decision-making processes, albeit in different ways, such as focusing on ownership or team composition.

Diversity in an asset class context

While diversity considerations are relevant to every asset class, not all of them can be approached in the same manner. Investor preferences can be harder to fulfil in some asset classes and sectors than in others, depending on what definitions are used. Ethnic diversity, for example, varies by both asset class and manager type (e.g. large publicly listed firms versus small privately owned ones), while gender diversity appears to vary by manager type and remain more consistent across asset classes.

Ethnic diversity varies by both asset class and manager type, while gender diversity appears to vary by manager type

In general, asset owners that focus on diversity have tended not to bring absolute expectations – although there are cases of mandates with explicit diversity requirements. More commonly, investors will look within a particular desired asset class or strategy and then, depending on the ‘lay of the land,’ take an appropriately contextualised approach that aligns their diversity philosophy with the manager universe.

In the same vein, we take a closer look here at particular asset classes and strategies – in this article, unlisted infrastructure.

Infrastructure manager snapshot

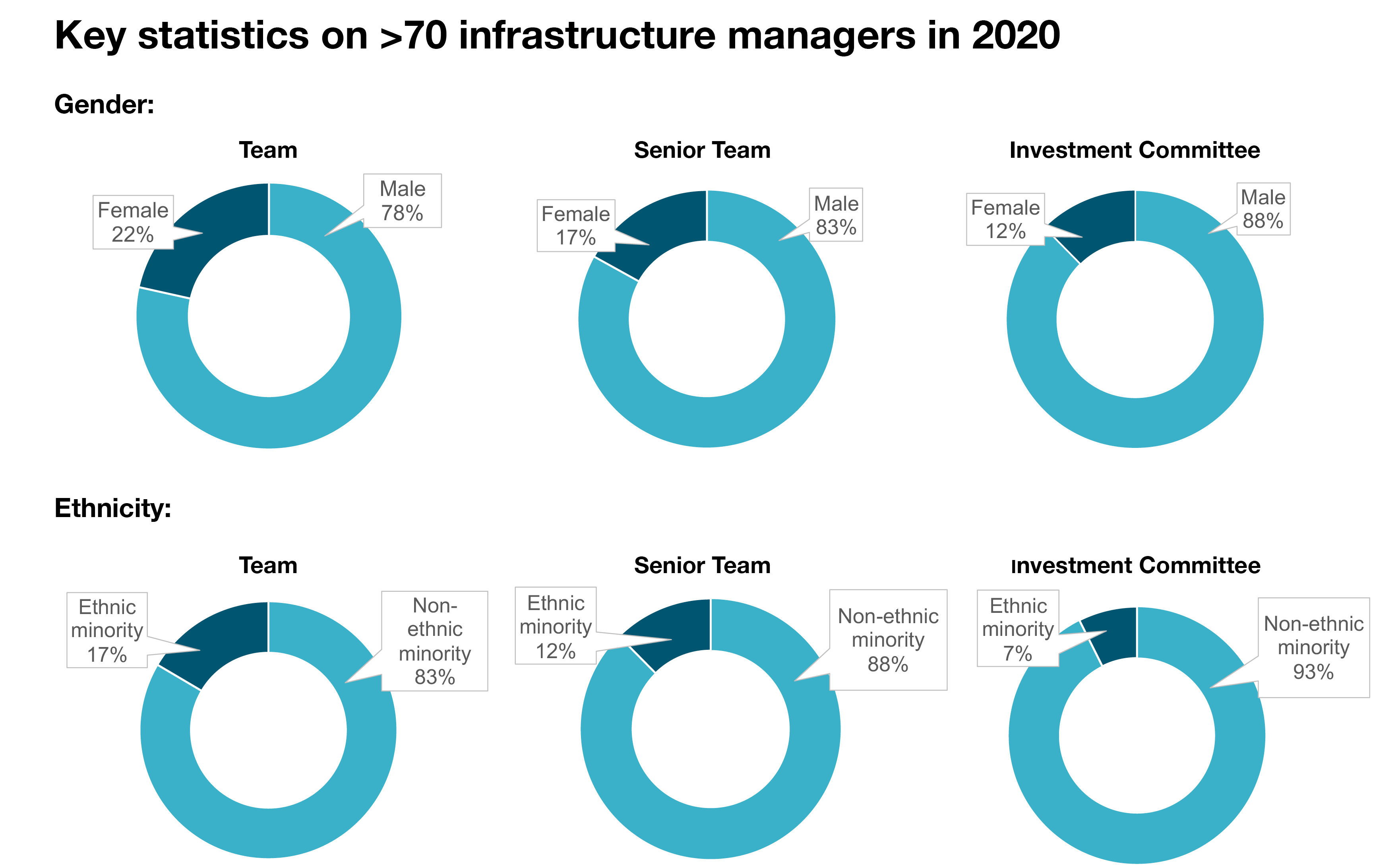

Diversity analysis is now included in all bfinance’s infrastructure manager searches, though the weighting assigned to this analysis varies depending on the investor. This includes assessment of the manager’s own team (including the overall investment team, senior team and investment committee, as illustrated below) and the way in which diversity is integrated into the investment process. In addition to the statistics on gender and ethnicity captured in these charts, it’s worth noting that 15% of funds have a female PM and 5% have an ethnic minority PM.

Anecdotally, we observe similar gender diversity in other illiquid asset classes, while ethnic diversity is a little lower in infrastructure due to the concentration of strategies in Europe and the US.

However, data can be a double-edged sword: box-ticking is endemic and the nuance lies beyond the numbers. Presumptions should be avoided: diversity policies do not necessarily translate into effective practices; team diversity doesn’t necessarily mean stronger consideration for diversity in the investment process; the list goes on.

What makes a good diversity policy?

A large majority of infrastructure managers have a ‘diversity’ or ‘diversity and inclusion’ policy. The lack of one is typically associated with firms that have less diverse teams, but the presence of a policy does not necessarily indicate that pro-diversity practices are prioritised or implemented effectively by the firm.

Only a handful of infrastructure managers have explicit targets on gender or ethnic diversity at their firm

Only a handful of infrastructure managers, for example, have explicit targets on gender or ethnic diversity at their firm – these tend to be the larger publicly listed firms who are increasingly implementing diversity objectives at board and/or senior management level. Examples include a 30% target for women on the firm’s Board of Directors, a 33% target for women at Operating Committee and Departmental Head level and a requirement that at least two diverse candidates are considered for each open role.

Another helpful differentiator is the frequency at which the diversity policy is re-assessed and re-endorsed; recent observations suggest that anything less than an annual review tends to be associated with weaker practices.

Diversity now versus ‘diversity momentum’

A firm’s current diversity figures are important, particularly for investors that view this subject through the lens of studies that have assessed the link between diversity and performance. Yet it is crucial to consider the context: a small Nordic manager, for example, will not have access to an ethnically diverse talent base in the way that a London-based or large global firm may enjoy, but may have the edge in their specific niches. Diversity looks different in different places.

Secondly, it is important to assess the ‘direction of travel’: we observe a significant number of firms where current diversity levels at senior level are very low but where recent hiring activity at junior- and mid-level has been more diverse, which can indicate a positive trajectory. Conversely, we see managers with senior female staff but lower-than-average gender diversity at junior levels.

Is diversity a firm issue, an investment issue or both?

We see relatively few cases where an infrastructure manager integrates diversity into their investment process and at the same time lacks a convincing approach to diversity at corporate level. Yet, we see many cases where the opposite is true – plenty of managers treat diversity seriously in their own businesses but do not appear to incorporate it as an investment consideration. Indeed, one can argue that it is less relevant in infrastructure than in strategies such as private equity, since investments are more “asset-centric” rather than “people-centric”.

If the manager's primary driver is to satisfy shareholders and tick boxes for clients then these outward-looking motivations may contribute towards a weaker approach

This may be (though is not necessarily) a ‘red flag’, even if an investor’s primary focus is the diversity within the manager’s own team. If a firm genuinely believes that having a more diverse team contributes to their resilience, innovation and success as a business then one may expect to see that reflected in the wider DNA and the way in which a firm views portfolio companies. If the manager’s primary driver, on the other hand, is to satisfy shareholders and tick boxes for clients then these outward-looking motivations may contribute towards a weaker approach.

We see a small-but-growing number of infrastructure managers with explicit targets on diversity within portfolio companies to be be achieved within a few years’ time, such as a manager who targets 30% diversity among all directors in the portfolio companies in which they have a controlling stake by 2023. Recent years have also brought the emergence of a sub-set of funds which explicitly target firms with diverse ownership; these vehicles are often geared towards US investors, where this subject has gained real traction – even with those who still find it difficult from a fiduciary and regulatory standpoint to pursue a broader ESG agenda.

Setting the agenda

We welcome the growing focus on diversity and the breadth of forms this takes across the global asset owner community. As understanding deepens, we caution both investors and managers against approaching this subject – and, indeed, ESG more broadly – with superficial box-ticking criteria. Instead, we would urge investors with a focus on this issue to prioritise the development of a clearly articulated philosophy on exactly why diversity matters to them. As well as adding impetus, this can bring clarity to cut through the challenging nuances of this subject.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.