English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  French (Canada)

French (Canada)

IN THIS PAPER

What is an impact strategy in private equity? Amid persistent definitional challenges, impact strategies should bear three key hallmarks: additionality, intentionality and measurement. The historic perception that impact investing requires accepting concessionary returns is rapidly becoming outdated with new evidence on performance.

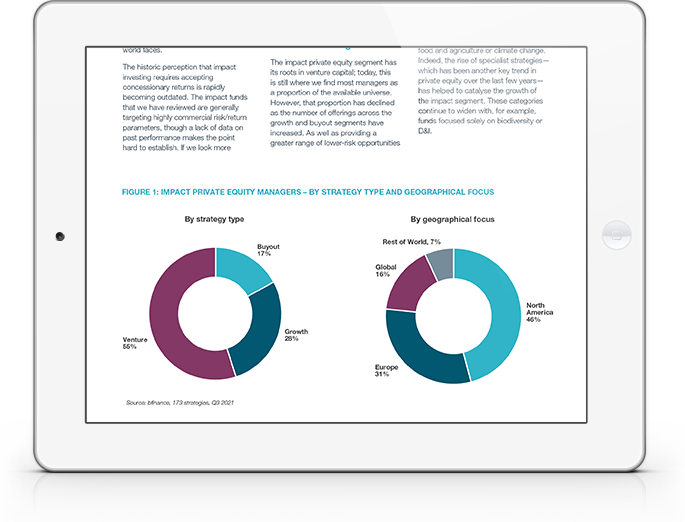

Available strategies and managers: Venture capital funds still dominate the universe but growth and buyout strategies have proliferated. We also note the emergence of secondary strategies, fund-of-funds and global (as opposed to regional) strategies as the market has matured.

Investment challenges include obtaining robust sector performance data, manager selection in a rapidly evolving product landscape, and scrutinising impact measurement methodologies with market participants increasingly cognisant of the need to avoid ‘impact-washing’. Investors can consider the pros and cons of making a discrete allocation to impact.

WHY DOWNLOAD?

There is an ever-growing opportunity for investors seeking to invest with an impact in private equity. The last five years has even seen some of the largest GPs such as Bain Capital and KKR introducing impact vehicles, raising funds worth multiple billions of dollars. Phenix calculates that 138 impact private equity funds were launched in 2019, followed by 73 in 2020. Placement agents that specialise in this area have emerged, demonstrating the maturation of the market and expectations for future growth.

Mapping the manager roster poses a significant challenge. The investment options are widening, in terms of both number and variety. An increasingly credible list of buyout and growth funds have emerged in a space that was, until recently, heavily dominated by venture strategies. Secondary funds are now available, as are fund of funds.

This brief introductory paper has been designed to assist investors that are considering this sector and seeking an understanding of the strategies, opportunities and challenges involved.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.