English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  French (Canada)

French (Canada)

bfinance insight from:

Chris Stevens

Director, Diversifying Strategies

Multi-asset fund performance has been under fire in the first quarter of 2018. Many investors were left underwhelmed by 2017 results and journalists have been on the front foot, as exemplified in this painful critique from Financial News.

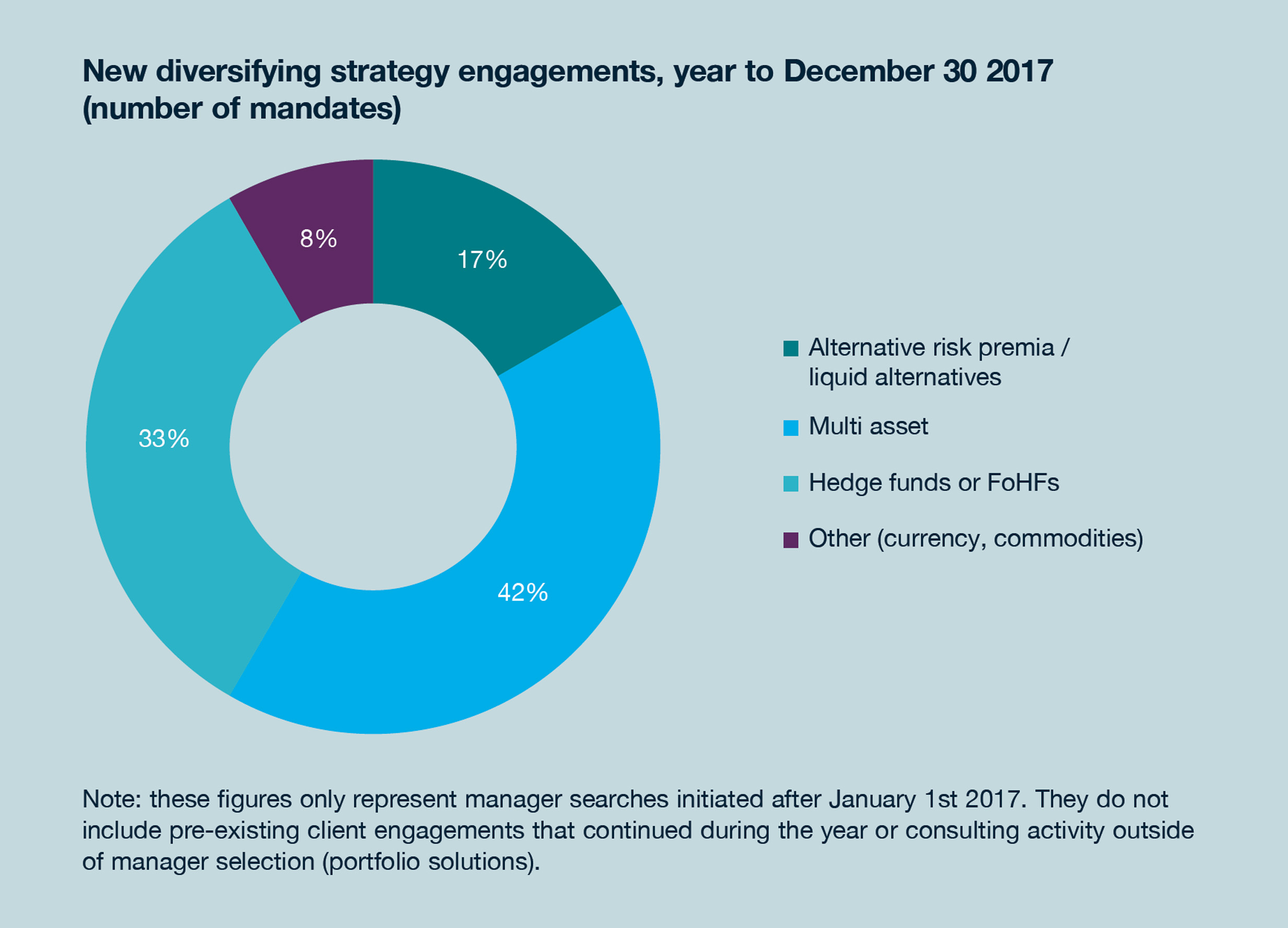

Yet, at bfinance, the appetite for multi-asset searches appears stronger than ever among our clients. This sector dominated new manager searches for Diversifying Strategies in 2017, outpacing hedge funds and FoHFs.

If we were to bring “Alternative Risk Premia” strategies into the Multi-Asset club, the number of mandates would outweigh hedge fund searches by almost 2-to-1. Such inclusivity is increasingly common, if a glance at the very diverse contributor list of this “2018 Multi-Asset Special Issue” of the Journal of Portfolio Management is anything to go by.

Increasingly, the most provocative question is not “how are multi-asset funds performing” but “what is multi-asset anyway?” The lines are increasingly blurred: this is a sector without clear boundaries.

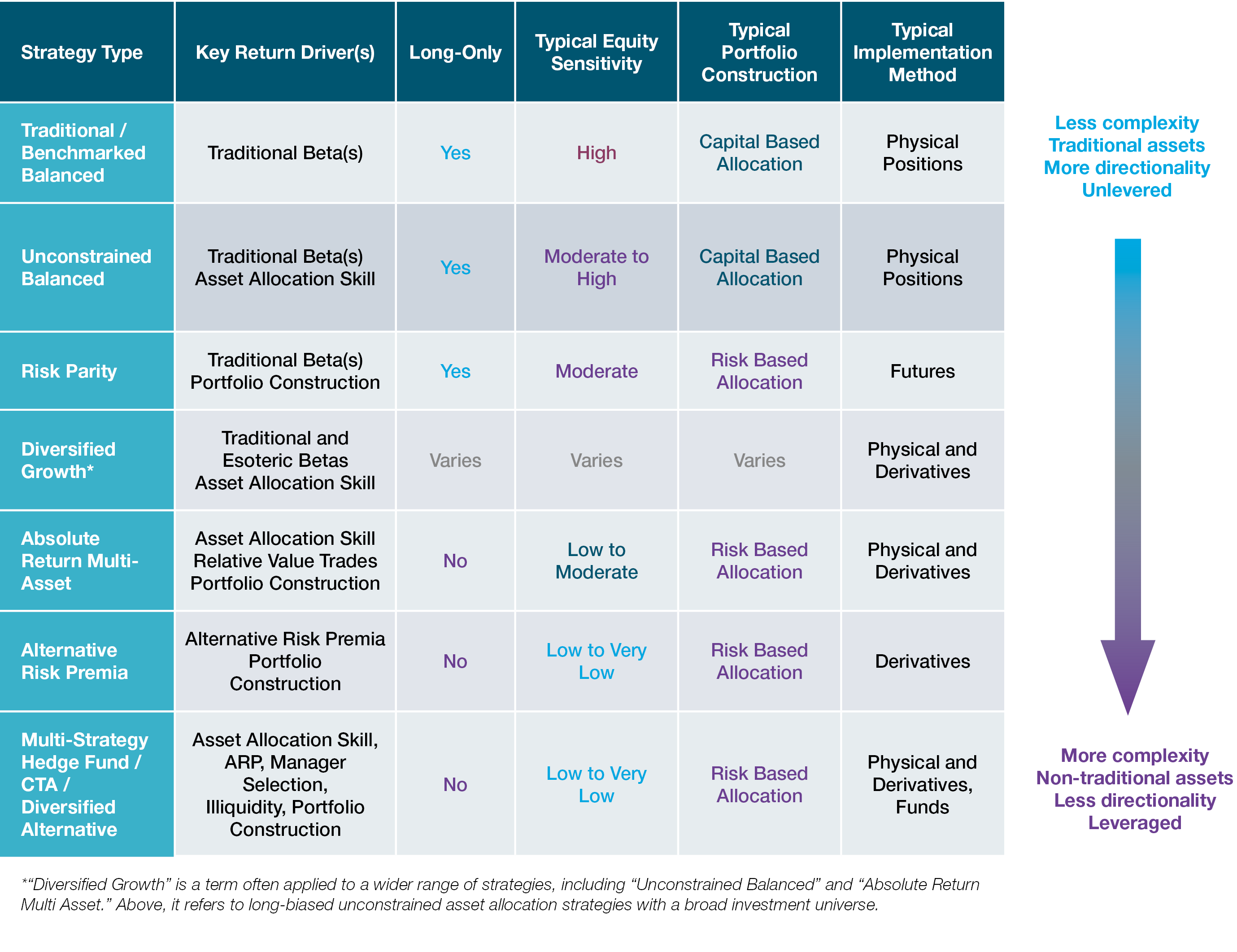

In our view there are seven meaningful categories of multi-asset strategy, although many more shades of grey can be found within and across these groups. The seven are illustrated below, in a framework designed to include all plausible candidates, from the traditional balanced fund first seen in the 1920s to the multi-strategy hedge fund. They lie along a spectrum: those with more traditional assets and more market directionality sit at one end; greater complexity and less directionality lies at the other.

This is not just a conceptual framework: it is a practical tool that we use to find out what clients really want, what they need, what their hard limits are.

It is particularly useful for weighing up competing priorities: diversification from equity, returns (level, and absolute vs. relative), volatility, actionable insights on tactical asset allocation for the in-house team. It allows us to dig into sensitivities and restraints around fees, leverage and complexity. This type of probing is particularly important given the diversity and heterogeneity of the sector.

1. TRADITIONAL / BENCHMARKED BALANCED

These usually seek to outperform a strategic benchmark (e.g. 60% MSCI world, 40% Barclays Global Aggregate) using a traditional long-only approach. Asset allocation is usually stable over time with tactical asset allocation and stock selection as value-add areas.

2. UNCONSTRAINED BALANCED

With an investment universe only slightly broader than the first type (e.g. adding credit sectors), typically they have a different objective: “equity-like returns” with lower volatility. With no strategic benchmark, the purest versions place few limits on minimum and maximum asset class exposures, except prohibiting net short or leveraged positions. Largely reliant on traditional beta risk, but with a greater emphasis on asset allocation as a source of returns.

3. RISK PARITY STRATEGIES

Rising in favour after the last financial crisis, these futures-based funds are named for their portfolio construction methodology. Rather than allocating capital to asset classes to achieve a return objective, they target equal risk exposures (usually to equities, rates and commodities/TIPS) with the aim of always having exposure to at least one asset class that is performing well. Portfolios target a specific risk level. Apart from group 6 and part of 7, these are the only “systematic” players in an otherwise “discretionary” landscape.

4. DIVERSIFIED GROWTH

The “Diversified Growth Fund” began life as a product targeted at UK DB schemes but has gained a wide global audience. They differ from their Unconstrained Balanced cousins in their greater use of (vanilla) derivatives and their wider use of non-traditional liquid asset classes (loans, ABS/MBS, listed real estate, listed infrastructure, commodities, insurance-linked securities, emerging markets etc). Although return profiles are smoother than Balanced funds, they should not be thought of as “all-weather,” being predominantly long-only and structurally long risk assets. Some target “equity-like returns”, others have a goal more in line with the Absolute Return category below (cash or inflation plus 4-6%).

5. ABSOLUTE RETURN

Distinct from DGFs for their lower equity sensitivity and greater complexity, this is the first category in our list that can plausibly claim to target positive returns in all market environments. As well as the typical “cash/inflation plus x,” many have low drawdowns as an explicit objective. They make use of short positions, both on an outright, directional basis and as one leg of relative value trades, with potentially significant notional leverage and sophisticated portfolio construction.

6. ALTERNATIVE RISK PREMIA

A newer addition to the space as a defined category, ARP strategies have been the focus of several bfinance papers over the past two years, clarifying the products and their performance. These are systematic strategies that make use of non-traditional techniques (shorting, leverage) to isolate risk premia (carry, value, momentum etc) in a generally market-neutral manner, across multiple asset classes (usually equity, bonds, currency and commodities).

7. MULTI-STRATEGY HEDGE FUNDS / DIVERSIFIED CTAS / MULTI-MANAGER DIVERSIFIED ALTERNATIVE

This final group is something of a catch all for alternatives-oriented multi-asset strategies. Single manager multi-strategy hedge funds and CTAs can offer exposure across a range of sub-strategies including equity long/short, futures trading, arbitrage styles and others. “Diversified Alternative” strategies are designed as a “one-stop-shop” for alternatives exposure, typically with a multi-manager approach (e.g. combining hedge funds with private markets allocations).

The Multi-Asset space is broad and deep. Investors can reduce the likelihood of missteps by considering the range of strategies that are available, the advantages and shortcomings of each, and then narrowing down this universe based on their real objectives and priorities.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.