English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada) - Australian Superannuation Fund

- 2021

- Public Equity - Small Cap

- AUD75 million

- Global Emerging Markets

- Seperate Managed Accounts

- Manager research

- >3% p.a. net return above benchmark

Our specialist says:

As was the case here, many investors are increasing their scrutiny of climate alignment and making formal commitments to net zero across their investment portfolios. This approach meant that managers’ climate alignment priorities—both at the corporate level and within the proposed investment strategies—formed a critical part of the review process. Typically, both EM and small-cap companies have more limited disclosure and ESG data available, but we found that many of our shortlisted managers were able to measure and report on carbon footprint data and some could even demonstrate insightful evaluations of companies’ transition readiness and climate-associated risks. That thoroughness paid off at the finalist meeting stage, when ESG credentials and climate change considerations emerged as one of the highest-priority topics of discussion with this client.

- 86Considered

- 31Long List

- 12Shortlisted

- 4Finalists

- 1Selected

Client-Specific Concerns

This client, an Australian superannuation fund, was making its first dedicated allocation to small-cap stocks in emerging markets (EM). The mandate was intended to serve as a high alpha component of the pension fund’s overall equity portfolio, hence the client’s aggressive return expectation of at least 3% net per annum above a relevant small-cap equity benchmark. The client’s investment team was also keen to ensure that any manager selected would be in line with the fund’s ‘net zero’ carbon emission commitment. To that end, the investment team wanted to find a manager that would a) be amenable to implementing a modified version of its EM small-cap strategy with a significantly reduced carbon footprint and b) meeting the pension fund’s other environmental, social and governance (ESG) requirements.

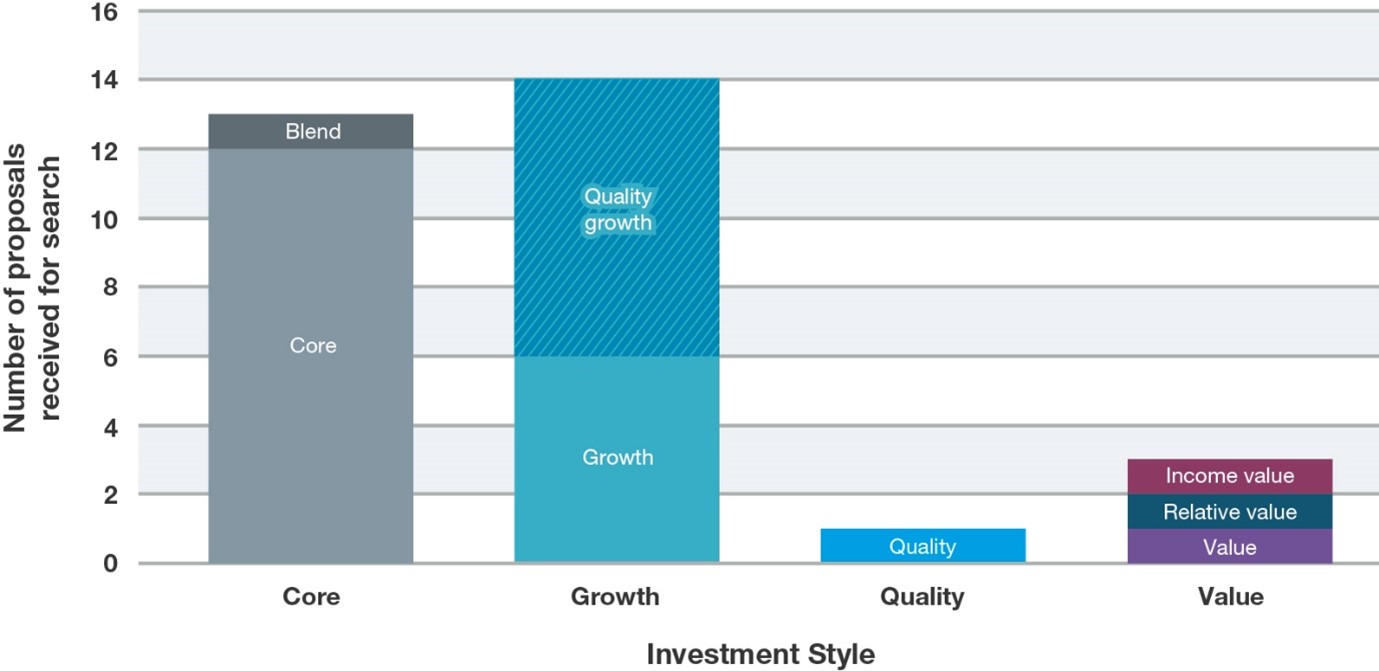

Number of Small-Cap Equity Strategies Proposed

Outcome

- Executing a targeted search: EM small-cap equity is an undeniably niche segment of the equity landscape, but—even after considering the client’s specific requirements—bfinance identified more than 30 relevant strategies for this client to review. The majority were discretionary fundamental approaches, however the four finalists included both discretionary fundamental and systematic/combined offerings. In terms of style, the most relevant strategies were Core, Growth, and Quality Growth, reflecting a bias towards Growth over Value in EM.

- Examining geographic weightings: inevitably, the manager search contained managers with different country-level biases; exposure to China, for example, ranged from 3% with one manager to 30% with another. Understanding these exposures was critical since the client needed to know how the small-cap mandate would sit alongside its other equity strategies (including a dedicated single-country allocation to China). With the outbreak of war in Ukraine, the managers’ exposures to Russia also came under review: at the time bfinance conducted the initial analysis in late 2021, exposure to Russia was generally modest across the EM small-cap funds under consideration (ranging from 2.5% up to a maximum of 6%).

- Determining manager ‘fit’ and complementarity: bfinance advised the client on how the prospective allocation would fit with its incumbent managers and overall portfolio, including the impact the new mandate might have on the risk/return and style profile of the overall equity portfolio. With input from our in-house Portfolio Solutions team, bfinance also evaluated different allocation scenarios to assess what EM small-cap weighting would be optimal for the prospective portfolio, and the best funding sources for the new allocation.

- Negotiated competitive fees: in light of increasing regulatory pressures on Australian superannuation funds to demonstrate value for money, the bfinance team assisted the client with fee negotiations throughout the search. This process included looking at both flat fee and performance fee options and executing quantitative value-for-money analysis by evaluating managers’ fees relative to the historical alpha generated by their strategies.