English (Global)

English (Global)  Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

A dramatic increase in the number and types of EMD funds available: Blended vehicles have gone from being a niche segment with barely 20 options to a rich universe of over 60. There is also more choice available in hard and local funds.

“Super-allocators” or “bottom-up blenders”? Investors seeking a EMD manager to swing tactically between local currency, hard currency and (often) corporate bond markets should be cautious with blended strategies. Exposure is largely driven by bottom-up country and instrument selection.

The challenge of assessing performance: With approximately a third of Blended EMD funds using an absolute return approach, benchmark-relative performance assessment is inherently problematic. Meanwhile, the large variation in sub-sector exposures makes comparison of headline track records misleading.

WHY DOWNLOAD?

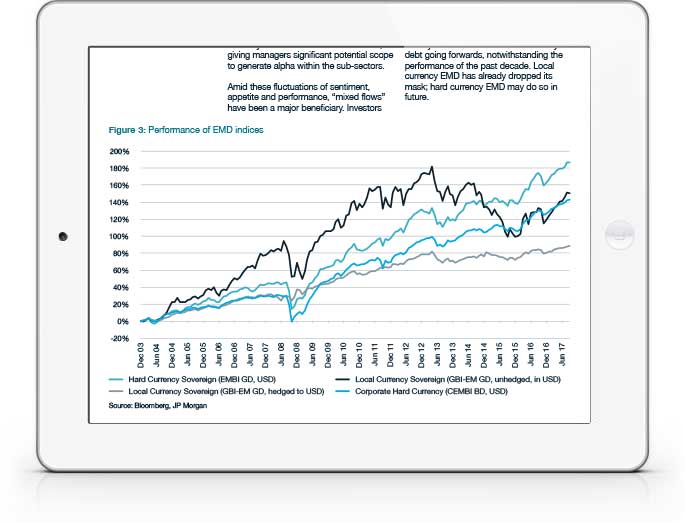

Emerging market debt has witnessed a dramatic return to favour since mid-2016, with fund flows exceeding the heights of 2012. Amid the fluctuations of sentiment, “mixed flows” have been a major beneficiary.

Information drawn from bfinance manager analysis in 2017 reveals insights about blended EMD funds. Investors seeking a “super allocator” to swing tactically between local and hard currency markets may have to think hard about implementation, with the majority of managers taking a bottom-up approach and a significant number showing little variation in sector exposures over a three-year period.

While these managers are outperforming relevant benchmarks by a modest margin, track records show greater success in reducing risk, with the average manager losing out on some upside but avoiding a significant amount of downside. “Absolute return” managers show lower capture ratios than their more benchmark-aware counterparts.

Performance analysis is a tricky task. A third of funds have no stated benchmark and there are no fewer than ten different benchmarks among the others. Absolute return analysis is required, but can be misleading due to the very different exposures to the relevant sub-sectors – differences that are often the result of process rather than tactical choice or “allocation skill.”

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.