English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada) - European public pension

- 2022

- Global equity

- USD 75 million

- Global

- Equity portfolio review & Manager research

Our specialist says:

A holistic review of an investor’s equity portfolio can help identify biases or gaps in sector, geographic, or factor exposures. As external manager line ups are often built up over time, market trends, performance and flows can affect allocations such that unintended biases or even style drift can creep in. Ideally, we want to see a manager roster which balances sensible diversification with high conviction manager selections, and evidence that each strategy is playing a distinct role with a meaningful contribution to the investor’s end portfolio.

- 325Considered

- 31Long List

- 8Shortlisted

- 2Selected

Engagement at a glance

The investor, a European public pension fund, was keen to conduct a review of their international equity portfolio, which included a roster of external active and passive managers. This confirmed an aggregate portfolio bias towards ‘growth’ at the expense of ‘value’ and ‘income’ and led to a manager search exercise to add a value style allocation to provide better style balance across the total portfolio.

Overall equity portfolio

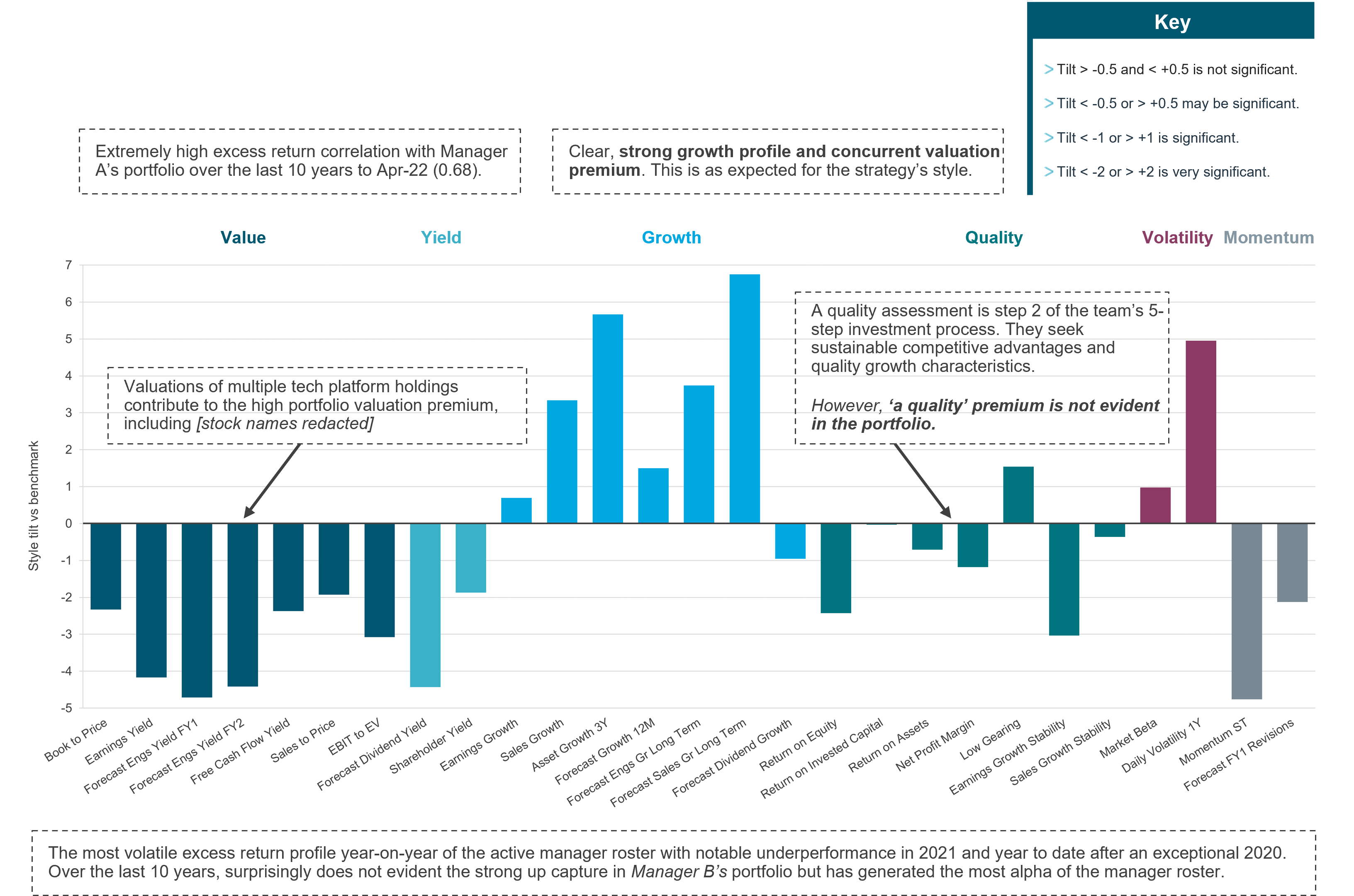

The review drew out evidence of how individual portfolio fundamentals were not always reflecting the expected style based on a manager’s espoused philosophy – such as ‘quality growth’ ultimately resulting in the investor paying up for high growth but without the commensurate quality:

Individual active equity managers

Style analysis Manager D

Source: bfinance, eVestment, StyleAnalytics. Based on latest available portfolio holdings data vs. MSCI World at Mar-22.

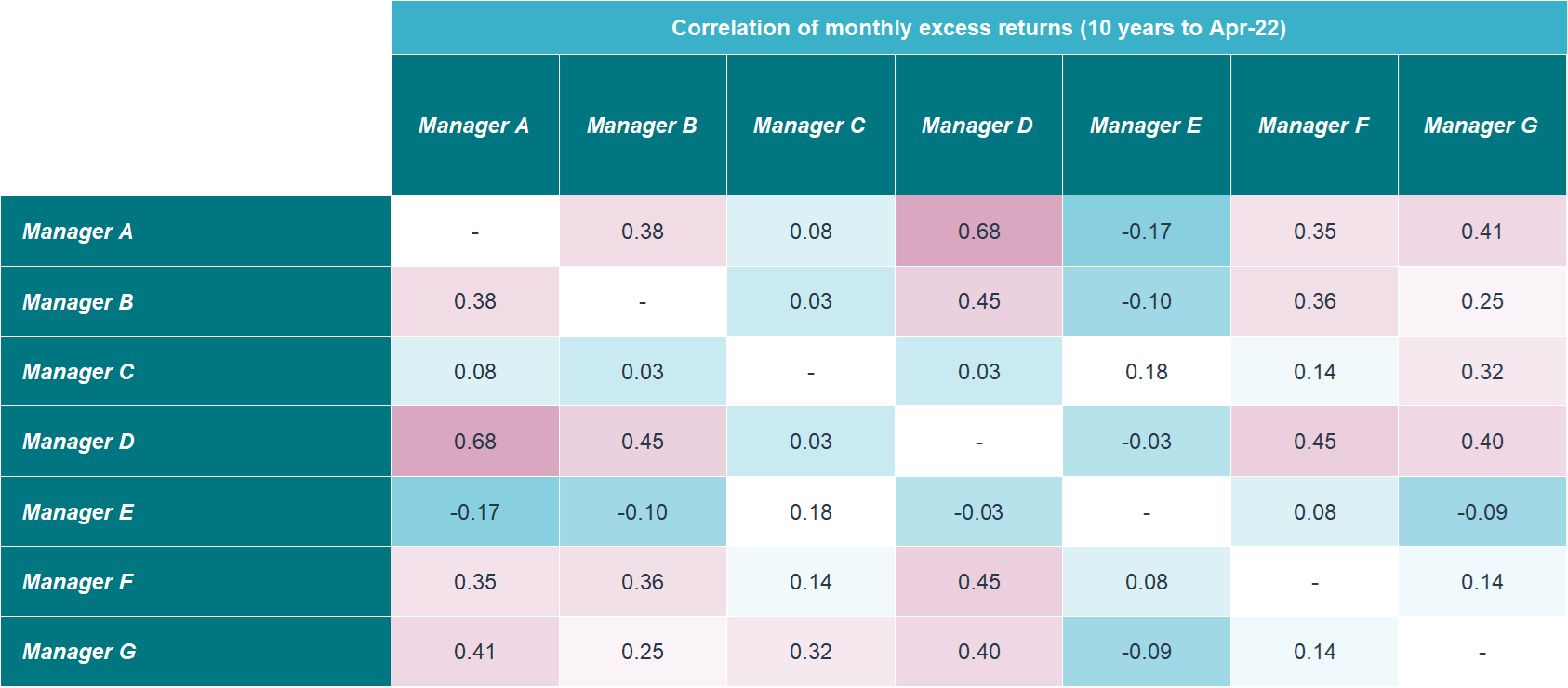

bfinance specialists reviewed the overlap across incumbent managers by weight, individual security names, and relative return correlation over time and drew on our knowledge of these managers’ approaches from our manager search experience to identify how the investor’s equity portfolio could be improved such that each manager allocation played a distinct, active role. For example, manager A and D stood out as having delivered remarkably similar relative track records over the prior 10 years, whilst others, such as manager E, had close to 0 excess return correlation with the investor’s other active managers, as indicated below:

Source: bfinance, eVestment, USD gross monthly strategy returns vs. MSCI World net returns.

Client-Specific Concerns

Amid a challenging market environment and in an attempt to crystallise its views on how its global equity portfolio could be improved, the pension fund sought an independent review and analysis of its equity manager allocations from bfinance.

The investor already had some insight on how manager changes over time had changed the shape and style of its equity portfolio. They were concerned about the representation of different styles in the portfolio and seeking an external manager roster akin to a football team that could balance aggressive offence, defensive elements, and core midfielders. bfinance’s role was to help evaluate the prevailing structure and any portfolio biases in order to provide concrete, actionable steps through which the external manager line up could be improved.

The client was seeking a pooled UCITS vehicle with at least USD 500 million in the proposed fund in order to meet its specific maximum client concentration requirements, linked to regulatory requirements for its jurisdiction. As the search progressed, the investor also sought to prioritise ‘defensive’ characteristics alongside clear ‘value’ credentials.

Outcome

- Customising equity portfolio review: Using portfolio holdings and track record data for the investor’s incumbent managers, bfinance experts analysed sector and regional exposures, style profile, carbon footprint, and track record characteristics at manager and aggregate equity portfolio level. This aimed to enfranchise the investor to understand current ‘gaps’ and how their manager selections could be improved and ultimately led to bfinance supporting the pension fund to implement a new manager search exercise.

- Looking through style headwinds: At the time of the manager search exercise, ‘value’ approaches had faced a medium-term style headwind. We took a deliberately long-term view (minimum 5-year strategy history) and evaluated performance against style-appropriate benchmarks. This was particularly important to avoid advantaging ‘relative value’ styles over ‘deep value’.

- Bolstering strategic defensiveness: With the prevailing market backdrop reflecting volatility and frequent style rotations, the investor was cognisant of defensiveness in market downturns. We assisted the investor in prioritising value managers which had a defensive angle in different ways – such as a low volatility value approach, or with an additional quality threshold for investments. From a quantitative perspective, we assessed strategy track records on metrics such as volatility reduction relative to the benchmark, down capture across a range of different bear markets, portfolio beta, and maximum drawdowns.

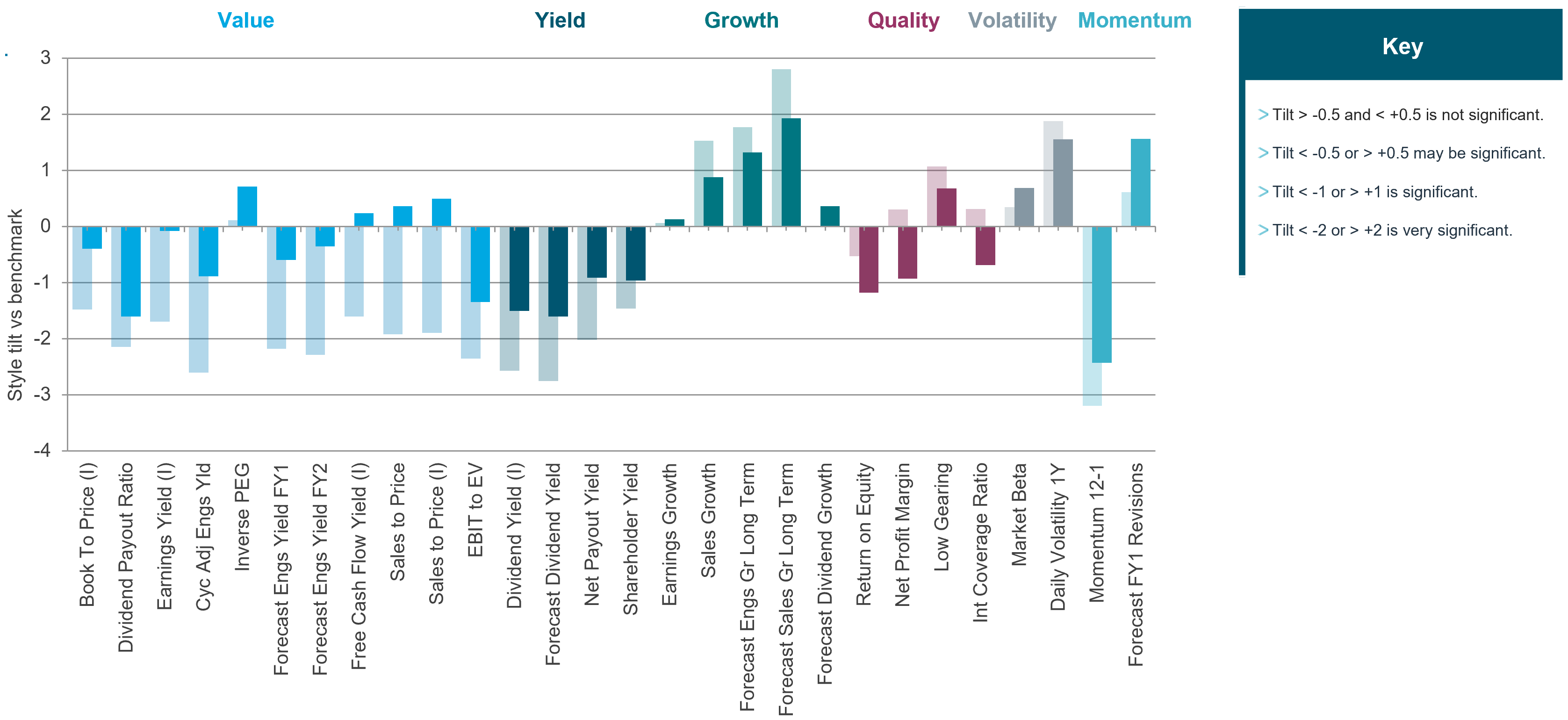

- Analysing various scenarios: bfinance conducted equity portfolio scenario analysis to show how preferred managers would fit with incumbents in order to compare complementarity of different solutions and identify if there were any obvious sources of funding to rotate into the new value allocation. Fees, client service, and scale efficiencies were also considered. This showed how a given allocation would moderate the style skews identified in the initial portfolio review, based on prevailing portfolio fundamentals.

Combination analysis: Scenario 3

Add USD Xm Manager 1, fund with USD Xm Manager B + USD Xm Manager F

Current portfolio (light shaded bars) vs proposed portfolio (solid bars)

Source: bfinance, eVestment, StyleAnalytics. Based on latest available portfolio holdings data vs. MSCI World at Sep-22.