English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada) - Northern-Europe Endowment

- 2023

- Currency hedging

- Strategic review of FX hedging policy

- Strategic Portfolio Design

Our specialist says:

Even static hedge ratio policies are an active portfolio decision and should be reviewed on an appropriate basis for suitability and efficacy in line with overall portfolio governance. Whilst more dynamic currency hedging solutions are more likely to produce optimal outcomes, they come with added complexity. In this instance, the client ultimately opted for a low complexity solution, but did so using our analysis to fully consider the range of available approaches and their individual strengths and weaknesses in the context of their portfolio.

Beyond devising a static FX hedge ratio across the entire portfolio and all foreign currencies, the analysis showed that the optimal hedge ratio is dynamic in nature and a function of FX rates, interest rates and local market pricing. Therefore, it would be possible to achieve superior results with an actively managed approach. Such strategies may also implement views on the global macro economy and use models to forecast expected returns for FX, interest rates and inflation which could add further value. This would require specialist expertise and an actively managed approach.

Client-Specific Concerns

A Northern-European endowment organisation engaged with bfinance to review its strategic approach for foreign currency hedging as part of its governance procedures. The investor wanted to review its existing strategic FX hedging approach and identify potential enhancements to better achieve its objectives of optimising portfolio-level risk-adjusted returns. The client’s existing framework required non-EUR FX risks to be 100% hedged for foreign currency exposures >2% of total portfolio. Hedging was applied across all asset classes, both public and private markets, and is implemented through the internal investment team.

bfinance supported the client by developing an assessment framework and therein assessing a broad range of portfolio hedging strategies in order to allow the client to make informed decisions.

Outcome

- Identification of strategic currencies Beyond devising a static FX hedge ratio across the entire portfolio and all foreign currencies, the analysis showed that the optimal hedge ratio is dynamic in nature and a function of FX rates, interest rates and local market pricing. Therefore, it would be possible to achieve superior results with an actively managed approach. Such strategies may also implement views on the global macro economy and use models to forecast expected returns for FX, interest rates and inflation which could add further value. This would require specialist expertise and an actively managed approach.

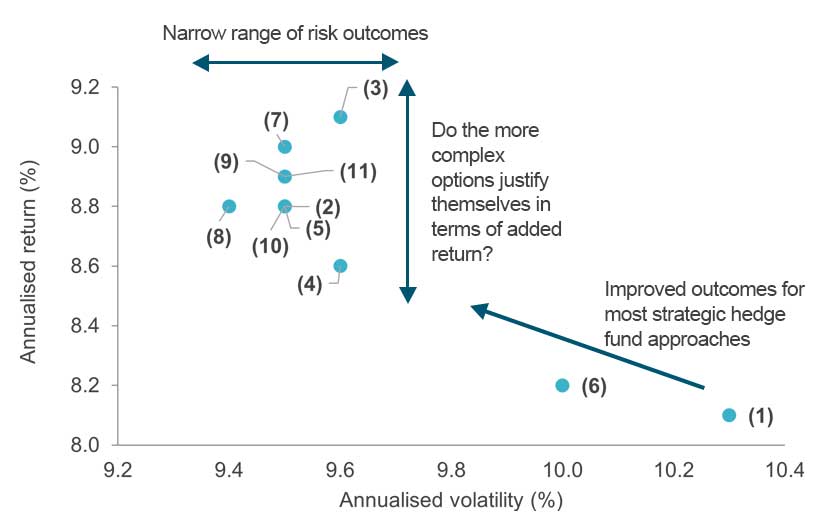

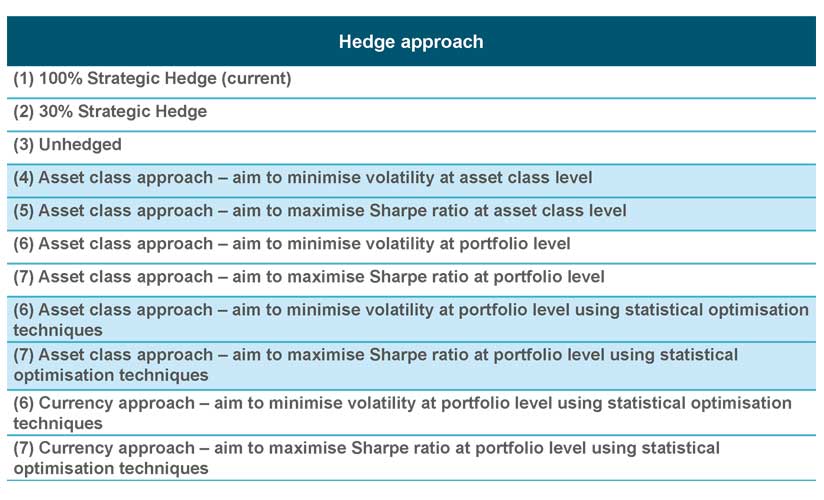

- Defining the problem: All currency hedging scenarios have three components: the asset classes being hedged, their currencies and the hedging ratio to apply. Different hedging ratios were considered for the strategic hedging approach, with the aim to uncover a potentially more optimal ratio from a risk/return perspective.

- Optimise the hedge level at the total portfolio level. Analysis showed that a 30% strategic hedge ratio applied across asset classes provided the best risk/return outcome for this client. This was a material shift from the client’s existing approach and substantially improved their portfolio outcomes. It appears to be challenging to substantially improve on the strategic hedge approach by individually optimising hedge ratios at the asset class or currency level – in those instances the diversification benefit across asset classes and currencies is ignored.