English (Global)

English (Global)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Peter Hobbs

Managing Director, Head of Private Markets

Today, investors in many illiquid asset classes are seeking subsectors and asset managers that can defy the overall yield compression of the last five years.

This case study is an extract from the recent bfinance white paper “Real Asset Debt: Lessons from Manager Selection."

An Australian superannuation fund was seeking to enter real estate debt in 2019 in order to improve the resilience and diversification of their real estate portfolio – then predominantly domestic and consisting entirely of unlisted equities.

The move was intended to improve downside risk and manage volatility in the event of a cyclical disruption, while providing sufficiently strong yields to avoid a significant reduction in overall returns.

Achieving returns of 4-5% with relatively low risk is not straightforward in today’s climate. As such, this investor was hunting for managers operating in less overheated segments of the market – managers who understand relative value and are able to be price-setters rather than price-takers.

The investor had some experience of private debt more broadly, having entered US and EU corporate debt two years before. Yet this was their first foray into real estate debt.

Home and away?

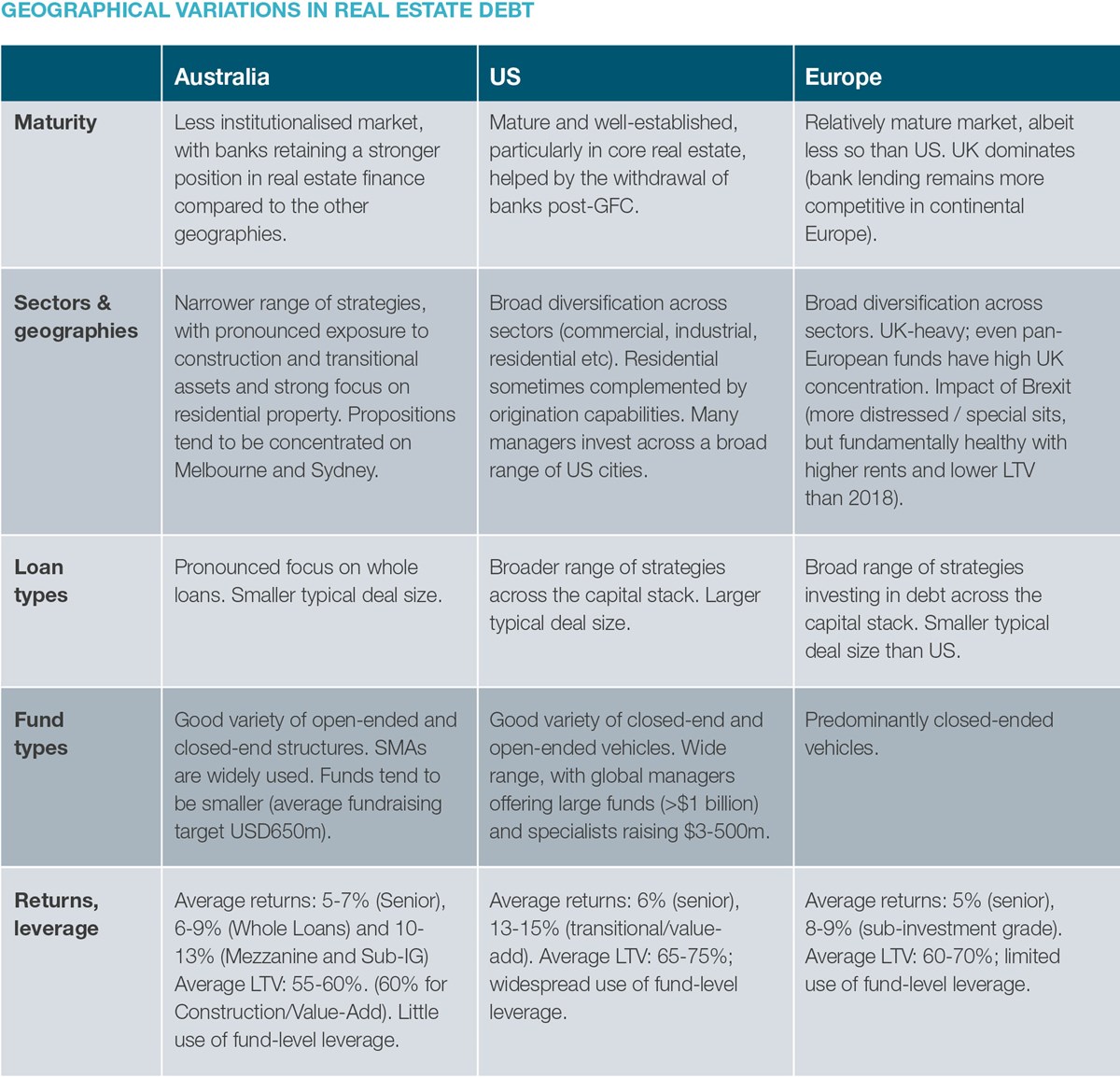

Initially, this pension fund was primarily interested in considering the US and European markets, since the bulk of their real estate portfolio was domestic. Yet analysis of the opportunity set within different geographies helped the team to reconsider this point and broaden the search to include Australia. Thirteen Australian real estate debt proposals were analysed in detail, alongside 20 in Europe and 20 in the US.

The Australian real estate debt market is proving particularly attractive right now in a global context. To some extent, this sector is now being supported by the same forces that have been at play in Europe for some years: a reduction in bank lending means that borrower demand has not been well serviced, producing opportunities for private capital.

Some of the most attractive opportunities in Australia at present involve smaller deals which do not tend to attract strong institutional demand or draw the attention of foreign GPs

ESG in focus

This investor is strongly committed to responsible investment principles and, as such, this search was designed around a distinctive set of ESG parameters. In particular, managers were required to provide feedback on the diversity – and particularly the gender diversity – of their investment teams and management. The client was particularly keen to see women represented on the portfolio management team.

Jargon buster

“whole loans” and “establishment fees”

“Whole loans” in real estate are broadly comparable to “unitranche” loans in the corporate direct lending sphere: a single, first-ranking loan which covers both the senior debt and mezzanine tranches and pays a blended return. Whole loans are secured against the real estate through a first-ranking legal mortgage. This type of loan has become increasingly popular, as have unitranche loans in the corporate sphere, with their ‘senior’ label and higher leverage; investors should examine the details of structures with care.

An “establishment fee” in Australia is similar to an “upfront fee” (or “arrangement fee”) in the US / Europe – a fee paid by the borrower to the lender when the loan is arranged, usually amounting to 1-2% of total loan value. Yet it is common practice for the upfront fee (US) to be shared with the LPs1, whereas the establishment fee (Australia) tends to be pocketed by managers alone.

Niche opportunity

Some of the most attractive opportunities in Australia at present involve smaller deals which do not tend to attract strong institutional demand or draw the attention of foreign GPs. This search yielded a substantial number of RE debt solutions from smaller (<AU$2 billion) Australian managers raising funds of less than AU$1 billion in size. Many of these also have real estate equity businesses and are willing to offer co-investments on the equity side to their debt LPs; this was particularly attractive to the investor, who ultimately selected two Australian managers that promised equity co-investment dealflow.

Seeking less overheated segments also proved critical in non-Australian manager research. In the US, investor demand for the large, well-established core real estate funds considerably outstrips supply; potential LPs can wait a year or more for access. The dynamics at the larger, more institutionalised end of the market are having a knock-on effect on returns, with yields squeezed and managers encouraged to employ more leverage.

The US manager that was ultimately selected is a smaller player with a strong focus on residential properties – particularly those with non-institutional sponsors, such as high net worth individuals purchasing apartment complexes or development projects.

The search for smaller, niche strategies has implications for the manager selection process. Some of funds that are particularly appropriate may score poorly on a number of conventional manager research metrics. It’s crucial to customise processes to investors’ priorities and avoid eliminating interesting candidates.

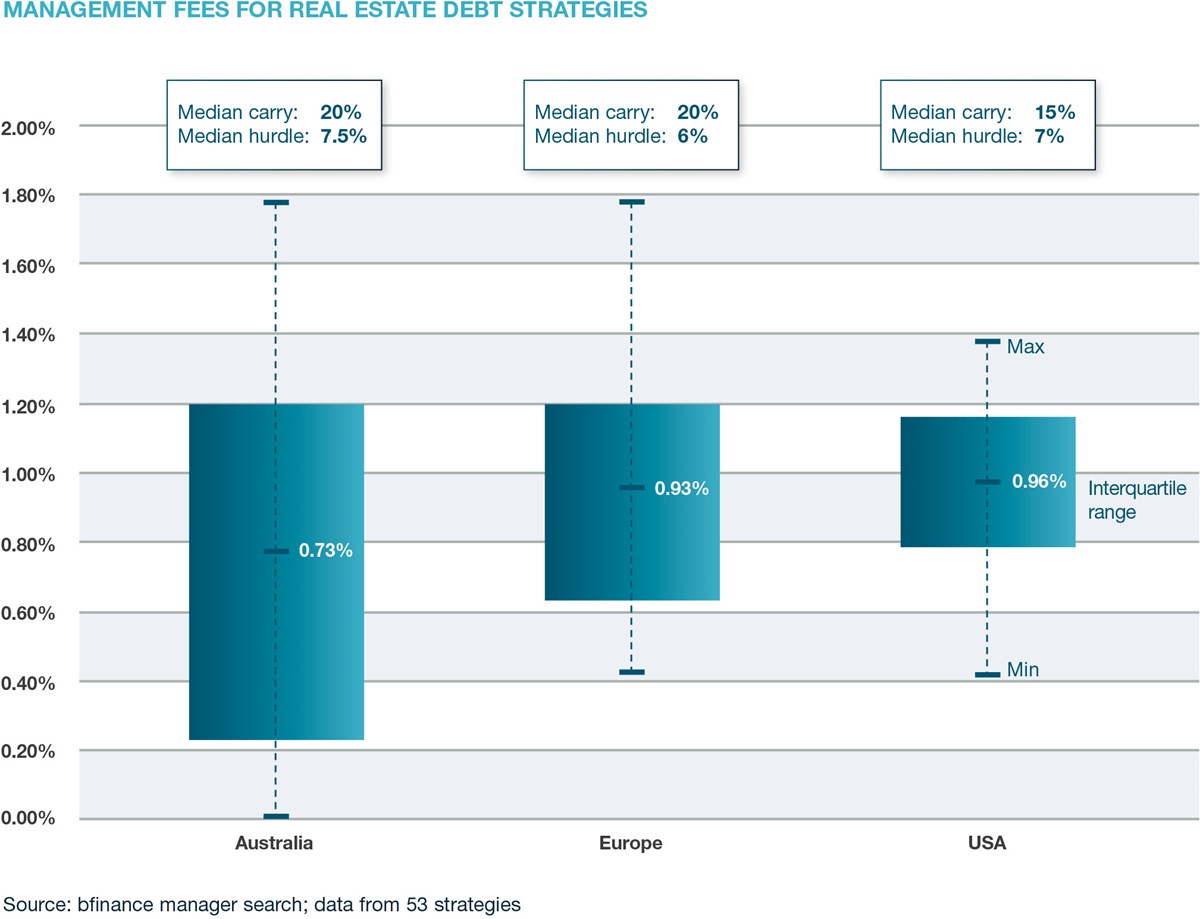

The cost conundrum

With a median management fee of 73bps, Australian real estate debt funds may appear to be cheaper than their US peers (median 96bps). Australian managers also appear advantageous from a carried interest standpoint: while performance fees in all geographies range from 10 to 20%, the hurdle rates that managers must achieve before carry kicks in tend to be slightly higher in Australia, despite the higher return expectations of US managers.

Yet true cost is a different story. Investors should bear in mind that a larger proportion of the leakage in Australia is hidden.

Under the country’s RG97 regulations, all fees and costs must be disclosed but anything skimmed off by managers without creating a visible “cost” is not reportable. For example, “establishment fees” paid to the manager by borrowers in Australia are not passed to (or visible to) clients, whereas “upfront fees” in the US are passed onto investors.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.