English (Global)

English (Global)  Français (France)

Français (France)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

In Late-July 2020, bfinance clients and other investors joined the research team (virtually, of course!) for a recap of active manager performance, portfolio positioning and investor activity in 2020 YTD.

In a first half that saw whip-sawing equity markets decline by over 20% in Q1 and rebound by 19% in Q2, many managers, strategies and factors showcased their ability to handle dramatic conditions while others were unseated by the nature or speed of market developments. Our senior researchers unpicked some details in a Mid-Year Review encompassing three sessions, available below:

Equity and Fixed Income (30mins)

- click here to watch

Diversifying Strategies and Risk Management

(30 mins) - click here to watch

Private Markets (30 mins)

- click here to watch

Below, you can find a few ‘editor’s highlights’ from the mini-series.

1) Growth was the only game in town for global equities

Active managers that have exhibited a strong Growth bias (as determined by bfinance) outperformed the MSCI world by 19.3% in H1, with managers deemed as ‘High Growth’ doing even better (Figure 1). Stock selection and style both contributed, with the MSCI Growth index delivering returns 6% higher than the MSCI World in H1. In general, equity risk factors (e.g. value, growth, low vol) have not produced the same pattern of returns that we’ve observed in previous crashes and recoveries: to find out why “This Time Was Different,” listen to Equity director Robert Doyle by clicking here.

Source: bfinance, eVestment, Style Analytics. Returns in USD, gross of fees, net total return basis

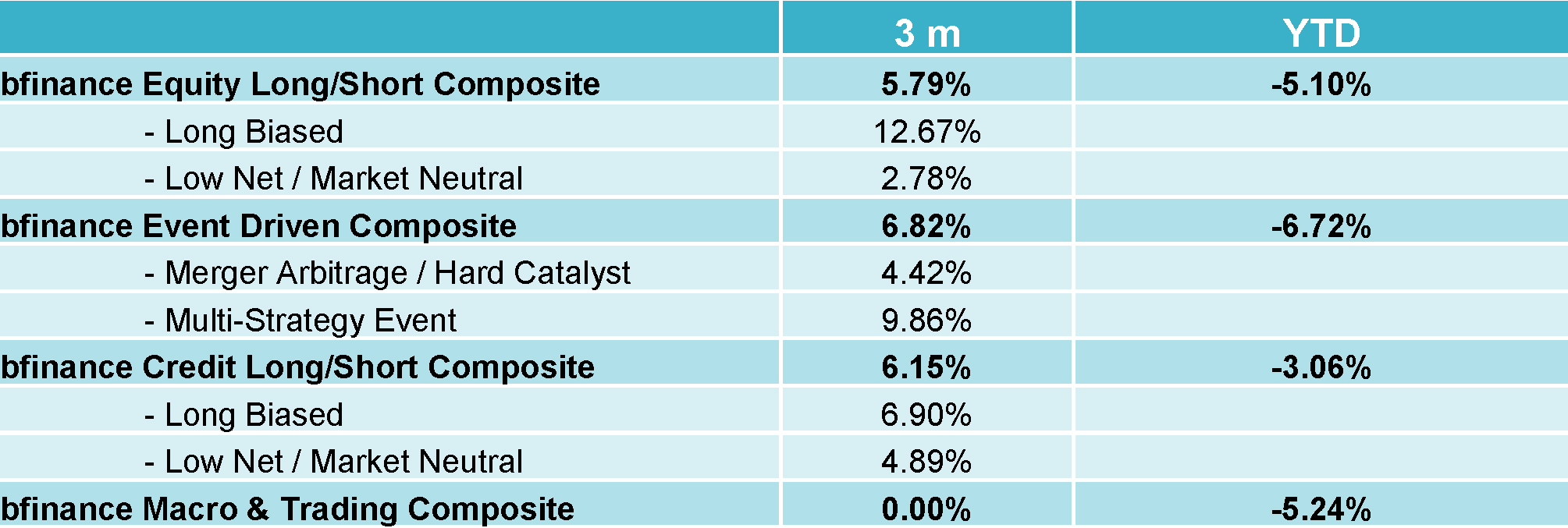

2) ARP’s annus horribilis tests investors’ faith in the asset class

Although there has been major performance dispersion within the various categories of alternative investment manager (i.e. hedge funds, multi asset), Alternative Risk Premia sat at the bottom of the pack in terms of average manager performance: -11.35% for H1 and -4.14% over the last three years. Although certain struggling factors made powerful negative contributions, portfolio construction, implementation details and risk management were critical to determining outcomes. With some funds already closing, 2020 will be a seminal year for this asset class. Hear more from Dr. Toby Goodworth (Head of Liquid Alternatives) and Chris Stevens (Diversifying Strategies) by clicking here.

Figure 2: [Table excerpt] Performance of alternative manager composites at 30th June 2020

Source: bfinance

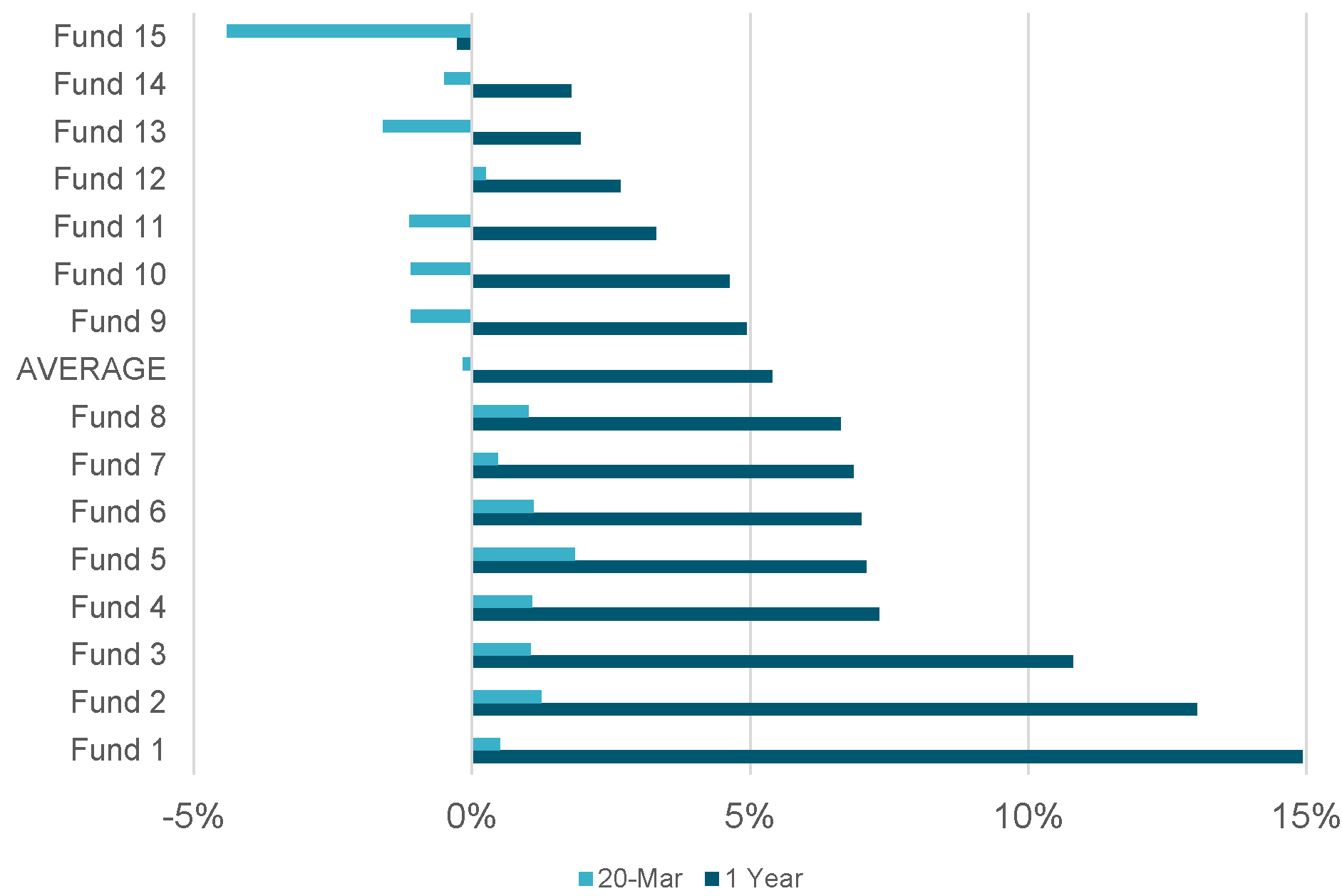

3) Private markets “winners” and “losers” start to emerge

It is still far too early to determine how asset managers across the key illiquid asset classes are delivering through 2020, but initial write-downs are already illustrating what we expect will ultimately be huge performance dispersion within sub-sectors. While results are of course driven by sectors and countries that are particularly affected by COVID-19 and the measures taken to combat it, there are also big differences in the performance of particular deals within affected sectors, illustrating the importance of discipline through the recent buoyant era. Valuations for Q2 are keenly expected during the coming days and weeks. Find out more from Peter Hobbs (Head of Private Markets), Sweta Chattopadhyay (Private Equity) and Anish Butani (Infrastructure) by clicking here.

Figure 3: Q1 valuation movement across 15 Pan-European Core/Core+ Funds

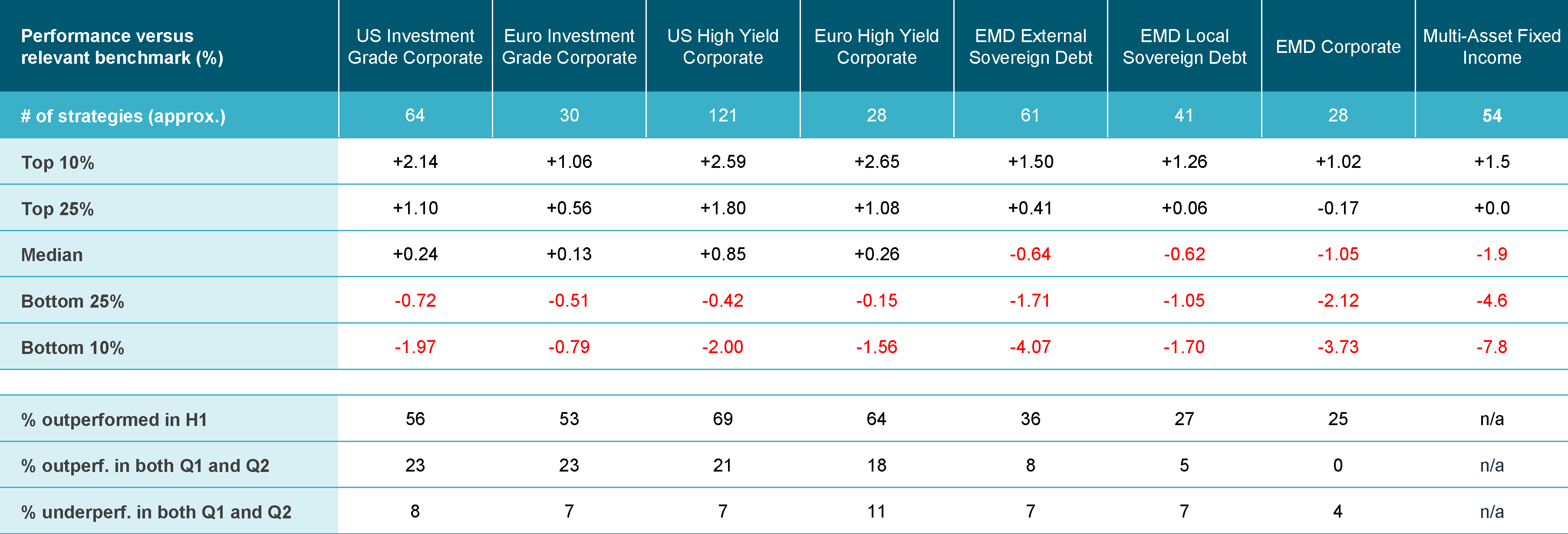

4) Data validates investor dissatisfaction with Emerging Market Debt managers

Active managers in Emerging Market Debt were one of the chief targets of investor disappointment in the July 2020 Asset Owner Survey. Manager performance data illustrates the notable H1 underperformance of median EMD managers versus their benchmarks, even after a strong second quarter: only 36% of EM hard currency sovereign debt managers beat their benchmark, and only 8% beat the benchmark in both Q1 and Q2; for local currency managers the figures were even worse at 27% and 5%. The oil supply shock, idiosyncratic defaults and – importantly – currency movements played a key role here. Find out more from fixed income director Kunal Chavda by listening here.

Figure 4: Performance of active fixed income managers relative to benchmarks, H1 2020 (gross of fees)

Returns in USD, gross of fees, 1 January to 30 June 2020. Source: eVestment.

Performance relative to benchmarks, except for multi-asset fixed income (absolute). Benchmarks: Bloomberg Barclays US Corporate, Bloomberg Barclays Euro Aggregate Corporates, ICE BofAML US High Yield, ICE BofAML Euro HY, JPM EMBI Global Diversified, JPM GBI-EM Global Diversified, JPM CEMBI Broad Diversified.

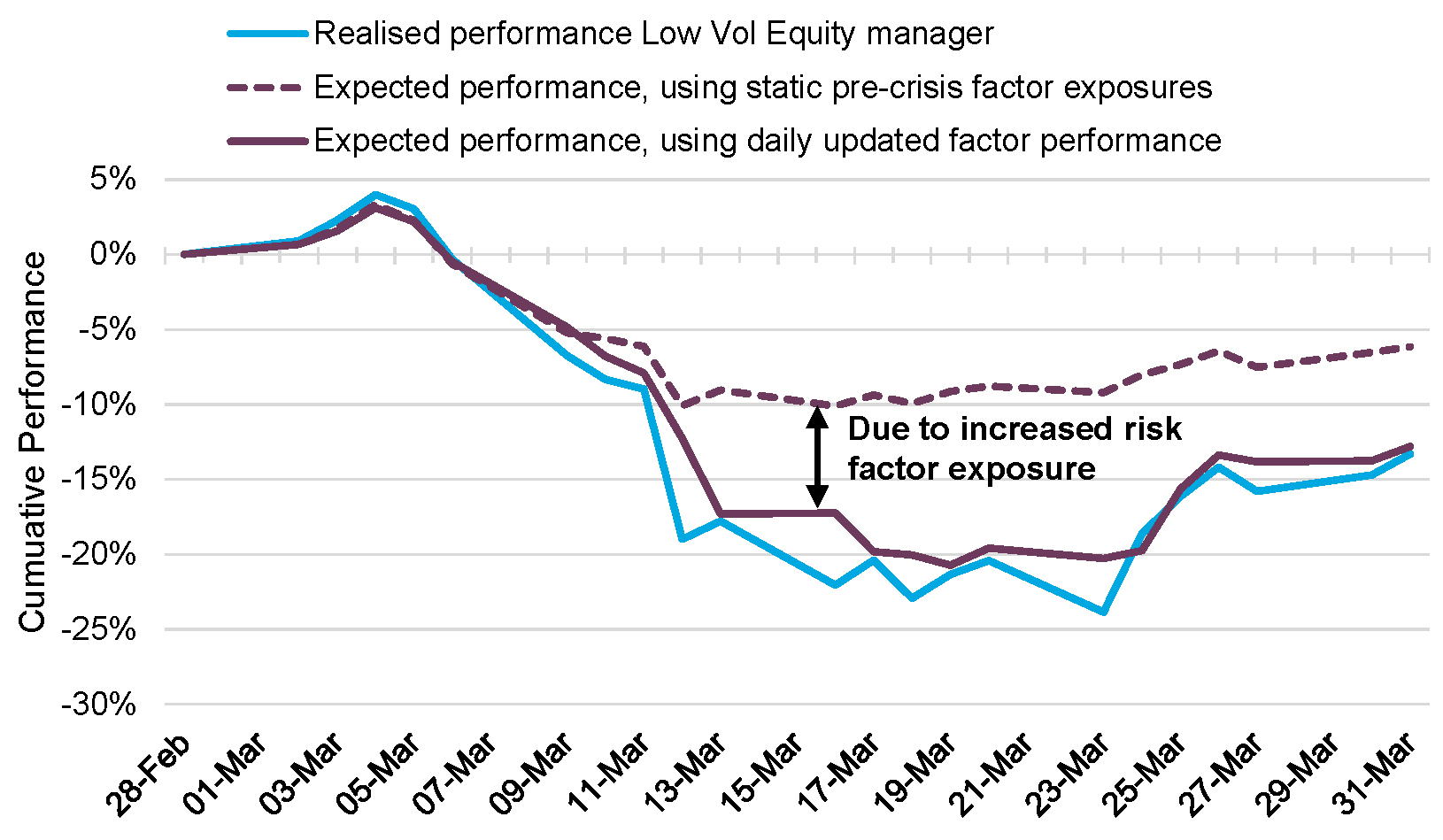

5) Crisis highlights the factor exposure challenge

Many strategies – active and passive – saw their risk factor exposures change dramatically over the crucial weeks in H1. A single-manager snapshot (Figure 5) illustrated the massive effect on performance as a Low Volatility manager saw their exposure to the Equity Risk factor (market beta) rocket from less than 0.7 to nearly 1. To find out more from Ruben Mutsaers (Risk Solutions Manager), click here.

Figure 5: March 2020 performance reconstruction for a Low Volatility Equity manager using risk factor analysis

Source: bfinance, Bloomberg

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.