English (Global)

English (Global)  Français (France)

Français (France)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

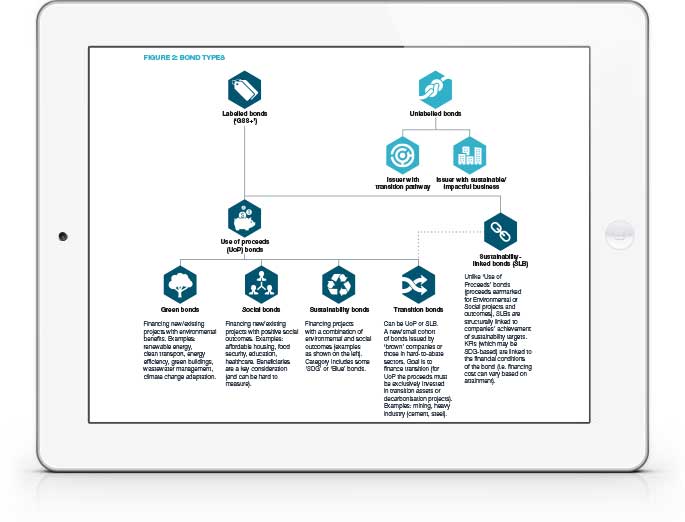

About the asset class. A clear run through the main categories of ‘labelled’ (GSS+) and ‘unlabelled’ bonds, with key facts and figures on issuer types, geography, credit quality and relevant sub-categories.

Investment strategies and evaluating managers. There are now 80+ strategies available to investors (majority active), including 45+ environment-focused active strategies and a meaningful minority that focus on social or broader impact. The past two years have seen a period of consolidation, with a slowdown in new launches as strategies mature and seek to build up assets.

The greenwashing challenge. GSS+ bonds are theoretically well-suited for sustainable and ‘impact’ investment. Yet investors must tread carefully amid self-classification, loose voluntary frameworks and conflicts of interest. We still consider it advisable to take an active rather than passive approach; even among active managers there is considerable differentiation in terms of resources, screening approaches, due diligence, reporting and more.

WHY DOWNLOAD?

The global debt market—and the institutional investors whose assets underpin it—are hugely influential in the trajectory of climate change mitigation and adaptation. With ‘fixing climate finance’ established as one of the four pillars of the COP28 Presidency’s Action Agenda, how should investors view fixed income instruments and strategies with a more targeted focus on sustainability?

Recent years have brought key developments for the GSS+ (Green, Social, Sustainability et al) bond market and the dedicated strategies for whom such bonds represent a key (though not necessarily the only) opportunity set. The market is still in its infancy. Yet the explicit connection that these securities create between investment and action has provided an undeniable draw.

The total historic issuance of GSS+ debt surpassed USD 4 trillion in 2023, less than a year after passing the USD 3 trillion threshold. Today, the current investible market is around USD 2.5 trillion —making it similar in magnitude to the global high yield bond market. Issuance continues apace: the peak of 2021 (>USD 1 trillion issued) has not quite been matched in subsequent years, but the GSS+ sector continues to represent 13-17% of all issuance in 2021-3, up from less than 5% in 2018.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.