English (Global)

English (Global)  Français (France)

Français (France)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Robert Doyle

Director, Equity

Weichen Ding

Senior Associate, Equity

China A-Shares and All Shares equity managers broadly failed to outperform falling markets in the third quarter of 2021 – a disappointment that may surprise onlookers, given that active managers have historically generated outstanding relative returns in this asset class. Conversely, two thirds of Global Emerging Markets equity managers beat the benchmark. What is differentiating winners from losers through China’s drawdown?

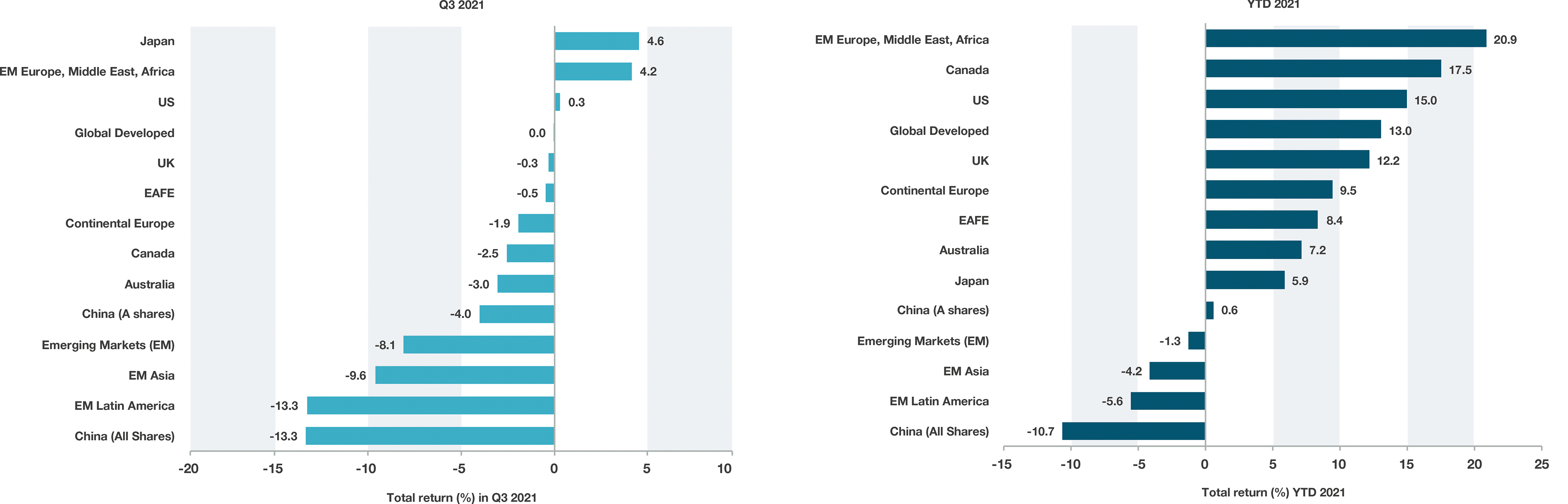

As discussed in bfinance’s Manager Performance Webinar (November 2021), the third quarter brought a very significant fall in China equity valuations, with the domestic A-shares market down 4% and the All Shares index—which captures a broader range of Chinese companies—down more than 13%. Given China’s direct and indirect significance to Asia and Global Emerging Markets, the decline had a significant knock-on effect on the MSCI Emerging Markets index (-8.1%) and Emerging Asia index (-9.6%). Several companies and sectors that are highly dominant in the Chinese market have struggled, including internet/e-commerce firms (with regulatory action against Alibaba and Baidu), education (TAL Education and New Oriental Education) and gaming (Tencent, NetEase), while the contagion surrounding Evergrande’s debt restructuring has grabbed some of the most dramatic headlines of the period. The sell-off had a minimal impact on developed markets, with domestically oriented headwinds having little direct effect on key developed market trading partners.

FIGURE 1: PERFORMANCE OF SELECTED COUNTRIES / REGIONS (MSCI)

Source: Bloomberg, data at September 30 2021. All performance data is gross of fees, representative median management fees for $100 million China A-Shares and Chinese equities mandates are 0.70% and 0.65% respectively.

Amid the turmoil, only 20% of active managers in China A-Shares beat the MSCI China A Onshore index in the third quarter, and only 27% YTD (at September 30). All Shares managers did a little better on a relative basis (48% have beat the benchmark YTD), though their benchmark has exhibited a far more dramatic decline. The picture for active managers in Global Emerging Market equities, however, is more positive: two thirds of them have beaten the MSCI Emerging Markets index during the first three quarters of 2021.

FIGURE 2: RELATIVE PERFORMANCE OF ACTIVE MANAGERS VS RESPECTIVE MSCI BENCHMARKS, YTD AT SEPTEMBER 30 2021

Source: bfinance, eVestment. All performance data is gross of fees, representative median management fees for $100 million China A-Shares and Chinese equities mandates are 0.70% and 0.65% respectively.

FIGURE 3: RELATIVE PERFORMANCE OF CHINA ACTIVE MANAGERS VS BENCHMARKS (ANNUALISED) – A LONGER-TERM VIEW

Source: bfinance, eVestment

The recent disappointing numbers for active management in China provide a very significant contrast against historic performance. More than 95% of A-Shares and All Shares managers have beaten their benchmarks over the last 5 years, with the median A-shares manager ahead by 9.5% per year and the median All Shares manager ahead by 5.4% per year.

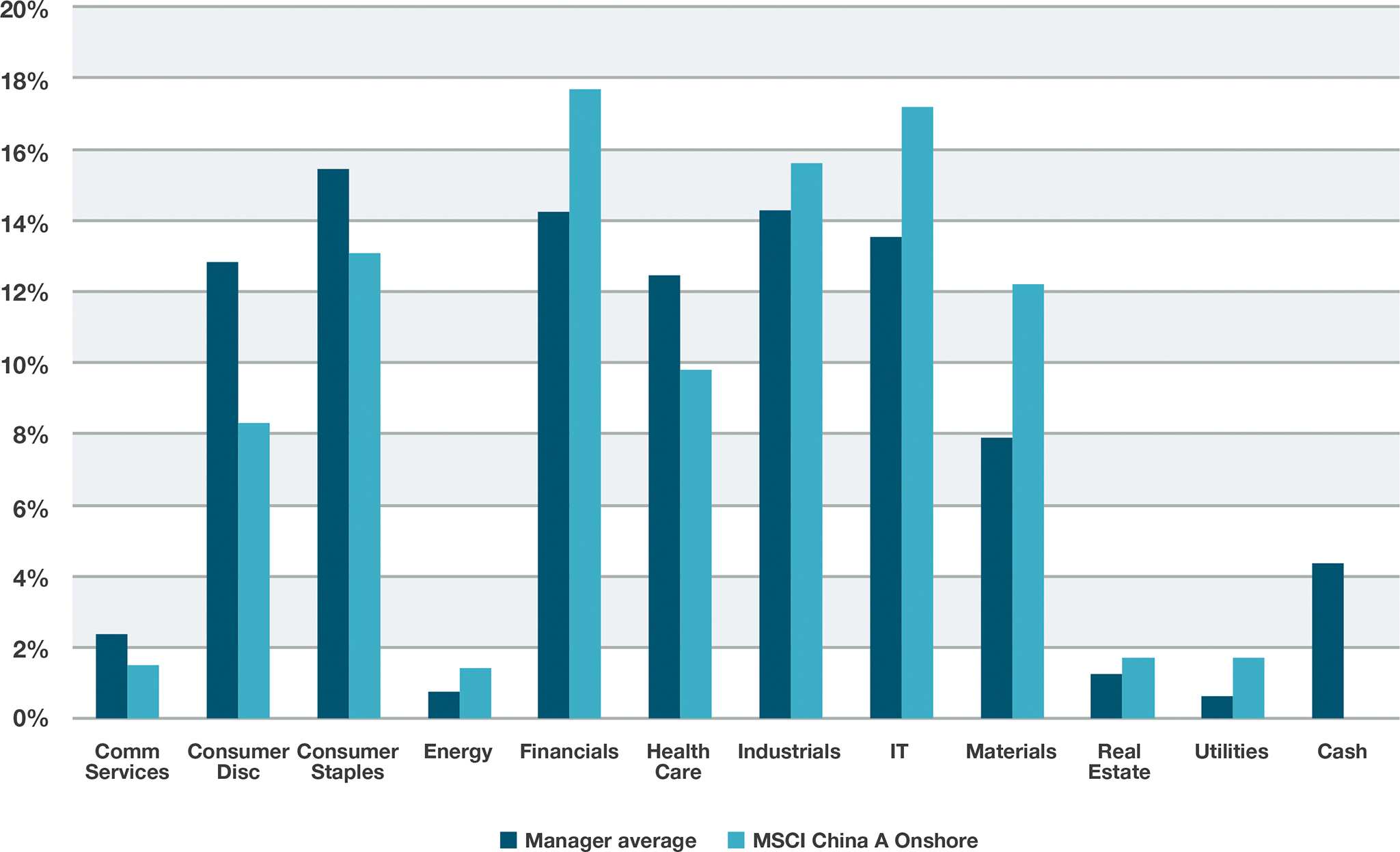

What’s the explanation for this dramatic turnaround in asset managers’ fortunes? One key factor to note is that China’s active manager universe, versus those in other markets, is heavily biased towards growth investing. This was particularly problematic in the third quarter, when growth companies struggled most, while financials, utilities and energy—sectors where China’s growth-focused managers would have little or no exposure—performed well. Analysis of a representative sample of China A strategies reveals that more than 70% have a discernible growth bias relative to the MSCI China A Onshore index, exhibiting higher rates of earnings and/or sales growth while being objectively more expensive using common valuation metrics. In addition, more than 80% have a discernible quality bias when viewing portfolios across a range of typical quality indicators

FIGURE 4: AVERAGE SECTOR EXPOSURES OF ACTIVE MANAGERS, CHINA A SHARES

Source: eVestment

The developments in China have also played a big role in the performance of Emerging Market equities more broadly. Recent months have been challenging for the Growth and Quality styles in Global Emerging Market equities and positive for factors such as Value, Dividend Yield, Quality and Size (small caps). Figure 5 illustrates the implications for real-life manager performance using a series of active manager composites developed by bfinance (sensible and representative groups of managers that have a strong leaning towards the named style). It's no surprise to see defensive Low Volatility managers doing particularly well during the Q3 downturn, although long-term relative performance has been weak. We also see very strong performance for the deeper value categories, where managers are typically underweight China—in part due to their low exposure to mega cap names like Tencent and Alibaba, which were specifically hit in Q3.

FIGURE 5: RELATIVE PERFORMANCE OF ACTIVE MANAGER STYLE COMPOSITES, EMERGING MARKETS

Source: bfinance, eVestment. All performance data is gross of fees, representative median management fees for $100 million China A-Shares and Chinese equities mandates are 0.70% and 0.65% respectively.

One surprise in these figures is the performance of the High Growth category, which many would assume to be heavily exposed to troubled stocks in Q3. In reality, many managers in this category have moved on from (or have underweights in) those mega cap Chinese companies, and generally are underweight China in favour of other Asian markets like India, Korea and Taiwan. The “core” group of Emerging Market equity managers also proved to be heavily exposed—these managers do not typically take big bets against a country such as China or the index heavyweights.

Another important driver of positive relative performance for active Global Emerging Market equity managers overall is their tendency to allocate (to a modest degree) to smaller companies, positioning themselves as underweight large and mega caps versus the index; it’s much more common for an active manager in this asset class to have an all-cap profile. Smaller companies have experienced a relative performance advantage this year, which has fed through into active manager returns.

Assessing manager performance

Overall, 2021 has (so far) been a strong year for the average active manager in Emerging Market equities, if not in China. From a practical perspective, however, institutional investors are more likely to have been disappointed. Pension funds and other institutions tend to be more heavily allocated to the Core, Quality and Quality Growth groups—which have not fared so well.

We would encourage investors who are disappointed with the performance delivered by Emerging Market equity managers (or indeed China equity managers) this year to keep a close eye on the performance delivered by other managers with similar style/strategy profiles, rather than relying on comparisons against benchmarks.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.